Money is always a sensitive topic of conversation. More so when the people involved are your parents who have always seen themselves as the responsible ones in the relationship. But there comes a day when it may be necessary for you to step in to help them make the right decisions and manage their finances, and you need to be ready for it. Be respectful in the way you approach and deal with it. Here are some dos and don'ts when bringing up money matters with parents.

Assess if they are ready

When parents are financially independent, they are likely to be more resistant to the idea of others (you) involving themselves in their financial affairs. They see it as unwarranted interference. You need to watch out for the signs that they are in need of help.

Common signs that tell you that they are ready include situations when you see them missing bill payments, forgetting and overlooking important details in financial transactions such as dates and signatures, avoiding and postponing decisions related to money because of which balances build up in the savings bank account, showing difficulty in following financial conversations and ideas, inability to understand risk in products and falling for dubious investment schemes and scams.

Plan the moves

This conversation is not going to be all done and dealt with in one sitting. If you know that helping your parents with their finances is going to be a part of your responsibilities, then it is good to start early. Plan how you will initiate it. Early interventions should be in the form of discussions about matters related to money on both sides.

One way to make it easier for them to allow you in is to offer to help with financial activities they don't enjoy doing. Taxes are a common bug bear, as are making investment decisions as they grow older. Another way to win trust is by introducing them to facilities and services such as online banking, systematic transactions and others that make it easier to manage their money.

Another way that may work for some would be to get a financial planner to talk to them. The professional nature of the individual may inspire confidence and allow access to their money affairs.

Get information

The first step would be to collect all the relevant information and documents essential to managing their financial affairs when they are there and later in the event of their demise. This includes information related to identity such as Aadhaar number, Permanent Account Number (PAN), details of bank accounts, insurance policies, investment accounts, property deeds, tax documents, power of attorney, passwords and other details that are necessary to managing money and accounts.

Check the names and signature on the accounts and documents and make sure that they match with what is currently in use. Sometimes a different way of writing names or applying signatures, even if the variation is minimal, may cause problems and are best dealt with when the concerned people are there to make the corrections.

Do a fit check

Your parents' need for liquidity, income and growth will change through their lifetime. Align the investments held to their needs. Weed out investments that serve no purpose and are either excessively risky or otherwise detrimental to their finances.

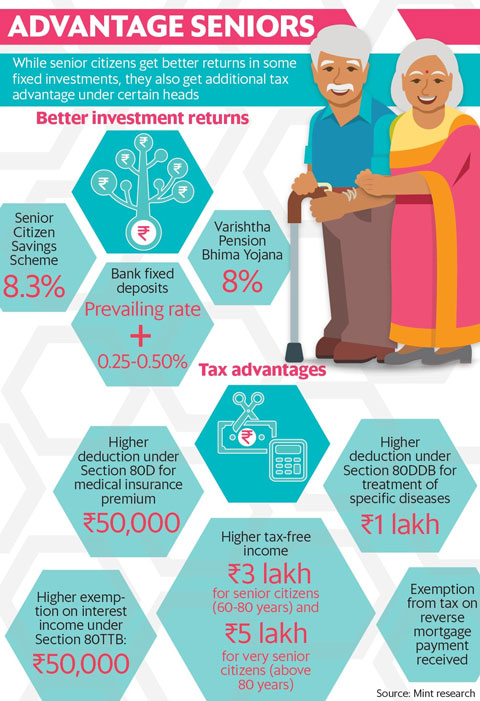

Keep the investments simple to evaluate and execute. Consolidate the investments so that there are not too many of them that simply duplicate the role that another is fulfilling in the portfolio. Take advantage of the higher interest rates that some products offer senior citizens and products that are designed to meet their needs such as the Senior Citizen Savings Schemes.

Similarly, evaluate the insurance policies for need and coverage. Eliminate those that are not required and add those that are required at their age and stage in life. Even if they are covered under your employer-sponsored health cover, evaluate if you need additional health cover and do it early.

If they don't have one already, encourage them to make a will. Help them make nominations in the existing investments as a first step. When they see how simple and non-threatening it is, it may encourage them to take up estate planning more formally.

Don't make any changes without your parents' knowledge and consent. Explain why you are making the changes and the impact it will have on their situation before you do it.

If the parents need your financial support, then it is a goal that you have to build into your financial plan early on. Preferences such as the need for independent accommodation, and whether there are siblings with whom you can share the responsibilities will need to be considered. Provide for their health needs early with insurance when they are reasonably healthy so that you don't have higher premiums and coverage issues later on. There are tax benefits on medical insurance taken for elderly parents and other health costs that you should make use of.

Don't behave as if you are doing your parents a favour by helping them with their finances or that they don't have a say anymore in how their affairs will be handled. Another sure-fire way to get their back up and make them resistant to your suggestions is to criticise the way they have managed their money. Not involving the rest of the family in decisions you are making can also be stressful for your parents. Handle the delicate situation by dealing them respectfully and patiently. Give them time to get used to the change and build confidence over time.

In arrangement with HT Syndication | MINT