According to reports, SEBI, the markets regulator, recently issued notices to certain mutual fund houses for selling small-cap funds, a high-risk investment over the short term, to super senior citizens (individuals over the age of 80).

Mis-selling of financial assets is an age-old issue. Even mutual funds are not untouched by this.

This unethical practice by some agents and distributors can have significant risks to all investors. It can be particularly damaging for senior citizens. Unlike younger individuals, senior citizens may not have the luxury of time to recuperate from financial setbacks, potentially jeopardising their retirement savings.

Therefore, it becomes imperative for investors, particularly the elderly, to arm themselves with the knowledge to navigate these financial traps effectively. Knowing what you want from your investments is key. Hence, in this article, we'll guide seniors through the steps they should take and share suitable investment options tailored to their goals.

Are you seeking a steady income stream?

If you're looking for steady income from your investments to cover expenses, you may have been pitched dividend plans, particularly from balanced advantage funds known for their dynamic asset allocation. These, however, may not be the ideal choice for a senior citizen as:

- These funds rely heavily on market timing, a risky endeavour even for seasoned investors.

- Dividends aren't guaranteed and are at the discretion of the fund house. Plus, dividends are not tax-efficient.

However, if you do want to invest in balanced advantage or dynamic asset allocation funds for ease of allocation, look for funds whose allocations do not swing wildly but rather stay within a narrow range.

What you should do

Opt for a systematic withdrawal plan (SWP) instead of a dividend plan.

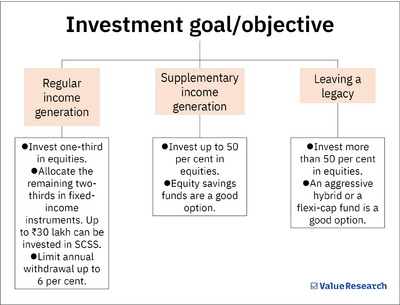

- Allocate one-third of your corpus in equities. They help generate inflation-beating income over time.

- Choose large-cap funds if you are conservative.

- Go with flexi-cap funds if you want a slightly aggressive approach.

- Spread your investment over two to three years.

- Allocate the remaining two-thirds of your corpus in fixed-income instruments.

- You can invest up to Rs 30 lakh in the Senior Citizen Savings Scheme (SCSS). It currently offers a guaranteed 8.2 per cent return annually.

- Invest the remaining corpus in short-duration funds for slightly higher returns than FDs.

Ensure that your annual withdrawal amount does not exceed 6 per cent of your corpus. Also, transfer a year's worth of required expenses in liquid funds, as they are much less risky.

Do you aim to create wealth besides occasional withdrawals?

For this goal, consider allocating up to half of your portfolio to equities and the other half to debt. Here's what you should do:

- Go for equity savings funds, as they offer a balanced approach with an average allocation of 35-50 per cent to equities.

- Alternatively, you can choose a 50:50 mix of debt and equity funds. Short-duration debt funds can provide stable income, while flexi-cap funds bring growth potential in equities.

Is your goal to amass a significant corpus for your heirs?

It is particularly relevant if you wish to leave a legacy, provide a financial foundation for your grandchildren's education or marriage, etc. This goal would generally require a time horizon of over five to seven years. Here's what you should do:

- If you are new to investing, consider aggressive hybrid funds, which invest primarily in equities with some allocation to debt.

- If you have experience in investing, opt for flexi-cap funds as they invest across market capitalisation and sector/themes.

- Invest via systematic investment plans (SIPs) instead of lump-sum investments.

In conclusion, by clearly defining your financial goals, risk tolerance, and investment horizon, you can avoid the trap of mis-selling and prevent yourself from losing your hard-earned money. Further, it is very important to do your own research, understand the product and associated risks, and then invest.