AI-generated image

AI-generated image

With the rising mercury, customers are crowding retail outlets for cooling products and investors are looking for stock ideas tailored to the season. One such name is Voltas , the market leader in the Indian air conditioner market.

With over 25,000 customer touchpoints, the Tata Group company was in news recently for being the first to sell over 20 lakh air conditioners in a single financial year (FY24). This was a 35 per cent jump over FY23. The feat was achieved thanks to Voltas' strong online and offline presence, new additions in stock-keeping units (SKUs) and its strong brand name. So far, it sounds like a solid summer play, right? But a deep dive reveals a different picture:

Running ahead of fundamentals

Despite being the industry leader with significant volume growth over the years, Voltas has struggled to maintain consistency in its profitability.

Voltas' financials at a glance

Inconsistent operating profit and shrinking margins

| FY19 | FY20 | FY21 | FY22 | FY23 | TTM | |

|---|---|---|---|---|---|---|

| Revenue (Rs cr) | 7,124 | 7,658 | 7,556 | 7,934 | 9,499 | 11,235 |

| Operating profits (Rs cr) | 577 | 654 | 607 | 644 | 533 | 456 |

| Operating profit margins (%) | 8.1 | 8.5 | 8 | 8.1 | 5.6 | 4.1 |

| Profit after tax (Rs cr) | 514 | 521 | 529 | 506 | 136 | 409 |

| ROCE | 16.8 | 17.2 | 15.1 | 13 | 5.6 | 7.2 |

| ROCE is return on capital employed | ||||||

Its revenue has grown a modest 8 per cent per annum between FY18-FY22 and the profit after tax has halved during this period. Surprisingly, the company is still commanding a searing valuation of 172 times.

Here's what is dragging the company's earnings:

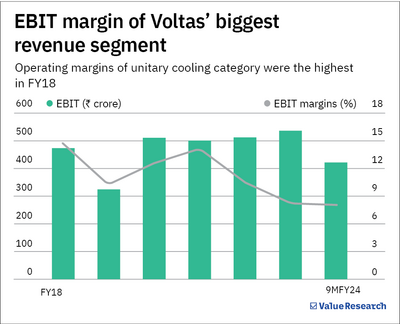

1) Shrinking margins in key air-conditioning category

Voltas derives the highest revenue from its unitary cooling products (air-conditioning segment). This includes room air conditioners (RACs), air coolers, commercial refrigeration and commercial air conditioning for both B2C and B2B clients. This segment accounted for 63 per cent of the company's revenue for 9M FY24. Notwithstanding the firm revenue and volume growth, the segment's operating margin has been on a downward trend.

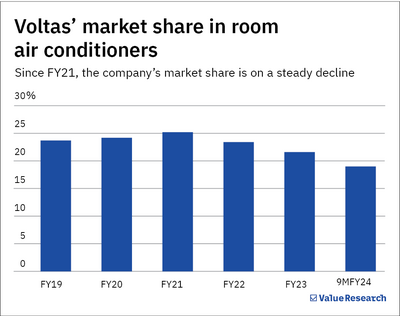

2) Competitive heat

This is due to intense competition, which has made it difficult for the company to increase prices in this category. The little to no product differentiation in the industry does not help either. As a result, Voltas' market share in RACs has fallen from 25 per cent in 2021 to 19 per cent as of 9M FY24.

Additionally, the company's housing appliance product line Voltas Beko, a joint venture with Turkey-based Arcelik launched in the second half of 2018, is yet to turn EBITDA positive. This is despite being operational for over six years and sold across 260 plus exclusive brand outlets. It aims to achieve EBITDA breakeven in 2025.

3) Headwinds in overseas projects

Voltas' second-highest revenue contributor is the electro-mechanical projects and services (MPS) segment, which undertakes engineering, procurement and construction (EPC) projects for domestic and international clients. The domestic business has been doing well, having grown 83 per cent in 9M FY24. But its international counterpart, with a significant exposure to the Middle East, has been a laggard.

Since the onset of FY23, the international segment has been facing cost overruns in ongoing projects and delayed payments from clients, forcing Voltas to make provisions. In FY23, the company incurred an exceptional loss of Rs 244 crore due to the termination of two overseas projects. The issue has persisted for the last 18 months with no relief until the latest quarter.

Overall, Voltas has incurred an operating loss of Rs 221 crore in the MPS category during 9M FY24. Notably, in these three quarters alone, this segment has lost more than it made in FY23 and FY22 combined. Its order book, as of Q3 FY24, was worth around Rs 9,000 crore but one-third of this came from overseas projects, which remains concerning.

Our view

The intense competition has crippled the entire industry's ability to maintain profitability in recent years. Voltas is no exception to this and it is safe to assume that the competition will not subside anytime soon.

The stock has been steadily rising on strong demand but the company's weakening financial metrics may catch up to it. Voltas has to expand its market share and strengthen its financials to justify its hefty valuations.