AI-generated image

AI-generated image

Just because it's popular doesn't mean it's the best. The same can be said of fixed deposits (FDs), an investment option that has maintained its popularity among multiple generations. As per the last SEBI survey in 2017, an overwhelming 95 per cent of Indians swore by FDs. Heck, even our prime minister, Narendra Modi, is an FD fanatic, holding 90 per cent of his assets there, according to the Election Commission of India.

The rationale is that FDs are safe and offer guaranteed returns. But if you dig deep, you'd find that they flatter to deceive.

Why? Their performance, for one, is underwhelming. Currently, the one-year SBI FD is delivering 6.25 per cent; in contrast, the average returns of debt funds, a similar risk-averse investment option, range from 6.1 to 7.56 per cent across various categories.

Since past returns don't guarantee future performance, we looked at the debt funds' yield-to-maturity (YTM). (YTM indicates the return if the fund is held until maturity.) Here, too, debt funds shine. For instance, short-duration funds would fetch 7.29 per cent returns, surpassing FD rates.

Debt funds also allow you to defer paying tax, where gains are taxed only upon selling the fund, unlike FDs, where interest is taxed annually. In addition, they offer greater liquidity and penalty-free early withdrawals.

Rate-cut benefit

Debt funds can also benefit from a decrease in interest rates. Many debt funds have an active investment strategy, so they can position their portfolios depending on falling or climbing rates.

For instance, when people expect interest rate cuts, long-term debt funds often steal the spotlight. The reason is simple: as interest rates drop, bond prices soar, with longer maturities seeing the biggest gains.

The opposite holds true, too. When interest rates go up, debt funds with shorter duration do well.

However, predicting the precise moment of a rate cut is next to impossible.

Take this year as an example. At the beginning of the year, there were widespread expectations of rate cuts. Anticipating this, many investors poured money into debt funds with a longer duration at the portfolio level. However, inflation in the West proved stickier than expected, thereby delaying the rate cuts. As a result, the higher-duration funds suffered the most.

What you should do

To avoid such surprises, it's better to invest in funds that don't overbuy longer-dated bonds. Which is why short-duration or corporate bond funds are two such categories that can be a better alternative to FDs.

While you can still consider longer-duration funds as a tactic, they should form a small part of your debt portfolio, as they can be more volatile than corporate and short-duration funds.

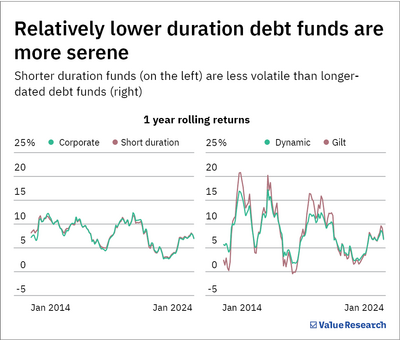

Let's take the example of popular yet volatile categories -- gilt funds and dynamic bond funds. Gilt funds generally invest in longer duration government bonds making them sensitive to interest rate risk. Dynamic Bond funds can invest in both long- and short-term bonds to take advantage of interest rate cycles.

If you look at their one-year rolling returns, you can see they are much more volatile than shorter-duration funds (such as short-duration and corporate bond funds).

Short-duration vs Corporate bond funds: The better option?

If you ask us, we will lean towards short-duration debt funds over corporate debt funds due to the following reasons:

- First, they must maintain a portfolio-level duration of one to three years, while corporate bond funds don't. This makes them safer than corporate bond funds.

- Second, short-duration funds invest in a mix of corporate and government bonds, implying they are less risky.

Also read: The range of debt funds