AI-generated image

AI-generated image

The FMCG sector has been down and out for a while now. Be it HUL, Marico or Dabur; all have struggled to generate double-digit volume growth in the past few years. This, combined with their high P/E ratios of at least 50 times, has subdued their share performance, too. But the star of our story, CCL Products, is head and shoulders above the rest.

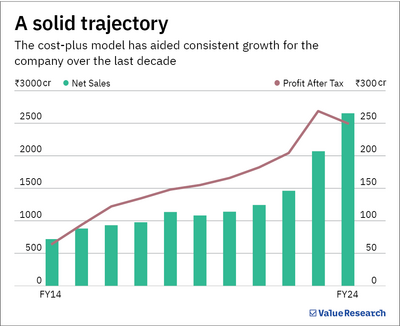

Its volumes have grown 10-12 per cent annually in the last decade. Notably, in FY24, they grew 14 per cent. If that's not impressive enough, the company has guided for high teens volume growth of 18-20 per cent for the next few years as well. The stock has shot up almost ten times in the last ten years, but trades at a reasonable P/E ratio of 32 times. Further, the company has a solid five-year median ROE of 18 per cent. The numbers make a compelling case, so we decided to decode the business and analyse its tall claims.

The business

While CCL Products majorly deals with B2C customers, it is still a close cousin of the FMCG family. It manufactures and distributes coffee products, mostly to global brands like Strauss Coffee and Jacobs Douwe Egberts. The company doesn't own any plantations. It only has factories that turn the raw coffee sourced from across the world into consumable spray-dried and freeze-dried coffee. Simply put, its end products are fast consumer goods.

That aside, the company works on a cost-plus model. Irrespective of the prevailing coffee prices, it sells the final products to clients at a fixed margin or EBITDA per kg. The company's earnings do not fluctuate with the change in raw material (coffee) prices. This also means unlike other FMCG companies, it does not benefit from the ease in input costs.

Sowing the growth seeds

CCL Products' confidence to achieve its bold goals stems from the groundwork it has been laying out. Here's what it is doing:

- Eyes on market share: The company aims to grab market share by providing cost-effective products to its clients. It is planning to drive the cost-benefit by leveraging its high technical know-how of blending thousands of varieties of coffee beans into final products. In 2023, it had an 8 per cent market share in the global coffee volumes and aims to increase it to 15 per cent in the next few years.

- Capacity expansion: The company is focusing on scaling up through a unique strategy. It is among those few companies that undertake their capex only when prospective clients are ready to purchase the output. Thus, CCL initially outsources manufacturing services for new clients. It's only when it's sure of retaining them and getting more orders that it undertakes expansion.

The company had a total capacity of 30,000 metric tonnes (MT) in FY17 when it decided to step up the capex. Between FY18-FY24, it spent around Rs 1,750 crore on capex, almost 1.9 times its cumulative operating cash flows for the same period. Its capacity was 71,000 MT as of FY24. It will now increase it to 77,000 MT by the first half of FY25. The company expects this increase to drive its volume growth closer to its guidance by FY27. That said, although the capex led to an over five-times jump in the company's debt during FY18-FY24, it remains manageable with the debt-to-equity ratio below 1, thanks to its strong cash generation ability.

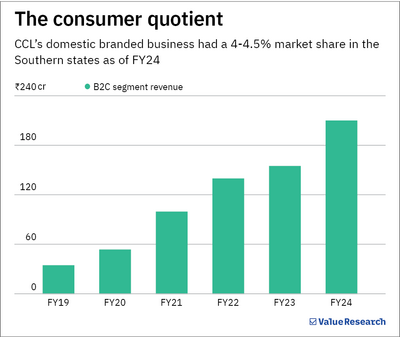

#Foray into B2C: More than 90 per cent of CCL's revenue comes from the B2B segment. However, the company has aggressively turned its focus towards the B2C segment or the domestic branded business, with the introduction of brands such as Continental Xtra and Continental Speciale. It aims to grow this category by around 30-40 per cent over the next several years. The business generated a revenue of Rs 210 crore in FY24 and is guided to touch Rs 350-400 crore in FY25.

The company has also been on a rapid acquisition spree in the last few years taking several B2C coffee brands under its belt, including Percol, Plantation Wharf, Rocket Fuel, and The London Blend in the UK market. In India, it was present only in the Southern states till now, but has begun expanding its footprint across the Northern and Western regions, too.

A flash in the pan?

On the face of it, the company's game plan looks solid. However, there are concerns that put the growth prospects to the acid test:

- Industry growth: It is quite difficult for CCL to keep growing at its current high pace when the global coffee market itself is growing at just 4-5 per cent, suggesting the sector has reached a matured state. High growth could be possible for small players, but CCL will be the second biggest player in the industry globally by output after its capacity expansion is done. Its plan to grow by gaining market share may need relooking.

- High coffee prices: Although coffee prices do not have a direct impact on CCL due to its cost-plus model, high prices lead to demand slowdown. This is already visible in the company's order book due to the current increase in prices. About 85 to 95 per cent of its targeted volumes usually get booked in advance at the start of the year. But for FY25, this has fallen to around 60 per cent, as some clients are hesitating to provide long-term contracts, preferring to stick more to two-three month-long orders.

- The B2C bet: CCL's consumer segment had been growing at a fabulous rate of 43 per cent per annum during FY19-24, mostly due to its low base and strong presence in the high coffee-consuming southern states. However, the business is still operating at a break-even level. The company is also in for stiff competition from existing renowned brands like Tata Coffee and Nescafe. It also does not have a significant cost advantage over peers to win consumers.

This story should not be construed as a stock recommendation. Investors must do their own research before making an investment decision.

Also read: 2x returns in 2 months: Is this stock a powerhouse or just a passing fancy?