India has historically traded at premium multiples compared to other emerging markets (EMs). On price-to-earnings (P/E) multiple, currently, it is trading at about 83 per cent premium based on consensus estimates. India certainly has been, and is projected to be, amongst the fastest-growing EMs (20-year real GDP growth of 6.5 per cent). However, GDP growth or even earnings growth, in and of itself, does not warrant a premium multiple or deliver higher returns. For instance, China has grown faster (20-year real GDP growth of 8.2 per cent) for a long time and yet has consistently traded at a discount. Further, its equity market has underperformed that of India over long periods measured in decades.

This is similar to what is observed for relative multiples of individual company valuations. As we all know, the company with the fastest-growing sales or profits in any sector or country does not necessarily merit the highest multiple. In fact, other factors, such as corporate governance and the quality of underlying assets, usually are the dominating factors that impact multiples. It should not be surprising if the same is true for the overall market multiple across countries. In this column, we discuss why India has deservedly traded at a premium because of superior country-level governance and underlying asset mix.

Governance factor

To state the obvious, the value of any country's equity market is the sum of the value of its constituent companies, which in turn is the present value of their future cash flows. By investing in a company's equity shares, an investor effectively buys the proportionate rights to its equity cash flows into perpetuity.

Where corporate governance is poor, there is a significant risk that cash flows would be diverted by controlling shareholders to the detriment of minority shareholders. As a result, the assumption of minority shareholders having a proportionate right to such a company's cashflows is weakened. It is not surprising, then, that such companies trade at discounted multiples compared to their better-governed peers. The weaker the governance, the greater the discount.

By logical extension, shareholder rights to the perpetual cash flows of equities would be more valuable in jurisdictions where such contractual property rights are less prone to being challenged by other parties, including the authorities, and where, if challenged, an institutional framework exists that provides fair protection to the holder of such rights (equity shareholders).

Countries with strong democracies generally have well-established independent institutions such as the judiciary, the central bank and the election commission, among others. Constitutionally, there exists a separation of powers between these institutions and the executive branch of the government of democratic countries. In well-functioning democracies, the separation of powers between these independent institutions and the executive branch of the government is enshrined in the constitution and operational in practice. Such an institutional framework can be thought of as the soft infrastructure of a country, which is essential to upholding property rights and maintaining economic and political stability. While such soft infrastructure is taken for granted in the developed democracies of the West, it is in varying degrees of evolution in emerging markets. We believe India is a more mature democracy than most other EMs and scores well ahead of them on this crucial soft infrastructure.

In many respects, India exhibits a more robust institutional infrastructure that is befitting of a developed democracy, with an independent judiciary, central bank, and election commission. There exists strong protection for property rights under the Common Law system, and institutional checks and balances ensure accountability of the government.

Without adequate separation of powers in authoritarian regimes, corporations and investors are exposed to a much higher risk of abrupt and arbitrary policy actions. Recently, we saw a regulatory crackdown on certain companies and industries and a general heavy-handed approach to dealing with businesses in one such economy. In certain resource-dependent EMs, there have been instances of asset expropriation. In many countries, foreign institutions and investors, particularly minority shareholders, have little recourse to appeal to protect their property rights.

It is not to say that there have been no disagreements between authorities and investors in India. However, what is different from many other jurisdictions is that corporations and investors, domestic or foreign, can expect fair hearing under the country's laws. A case in point is the tax dispute between a global telecom company and Indian tax authorities, in which India's Supreme Court ruled in favour of the former. There are very few other emerging markets where foreign companies or investors can file a lawsuit against the government, where they expect not only a fair trial from the domestic court but also to continue to operate in the country without any fear of vindictive repercussions.

Adequate institutional checks and balances have also given India the unique distinction of being among the few EMs with no instance of a currency crisis, sovereign default or political coup in many decades. Investments in emerging economies are often subject to such risks, as shown in Exhibit 1.

But, the absence of such debacles in India results from its robust soft infrastructure, reducing the country risk and contributing to its premium multiples.

In our view, one key reason India is consistently rated as one of the most democratic countries is the institutional separation of powers and the robustness of its soft infrastructure. As illustrated in Exhibit 2, India's Net Democracy Score ranks towards the top end of the emerging market peer group.

To summarise this aspect, governance must and does receive paramount consideration in any robust investing framework. The idea of governance at a country level encompasses numerous strands, each intricately linked to the other - is it a stable democracy or an authoritarian regime? What is the degree of institutional independence and separation of powers? Is the rule of law and property rights upheld by the judiciary?

The answers to these questions play a dominant role in determining the premium or discount investors ascribe to different emerging markets. As evidenced by the data of over 20 years in Exhibit 3, the markets in most democratic regimes have consistently traded at a premium to markets in the least democratic regimes.

Superior asset mix: Ownership profile and earnings stability

Even in an individual company, the quality of underlying assets has a significant bearing on the relative premium that investors are willing to pay. Similarly, markets where a larger proportion of underlying constituents are deserving of higher multiples would also be expected to have higher multiples at the aggregate market level.

In the EM context, government versus private ownership of a company has a significant impact on a company's multiple. Universally, it is observed that government-owned companies (SOEs or PSUs) trade at lower multiples as compared to their private sector peers.

Consequently, at a country level, a higher degree of state ownership in equity markets would result in a lower market multiple and vice versa. Countries like China, which generally trade at lower multiples, have higher SOE ownership than the EM average of 21 per cent. On the other hand, SOE ownership in India is one of the lowest at 12 per cent.

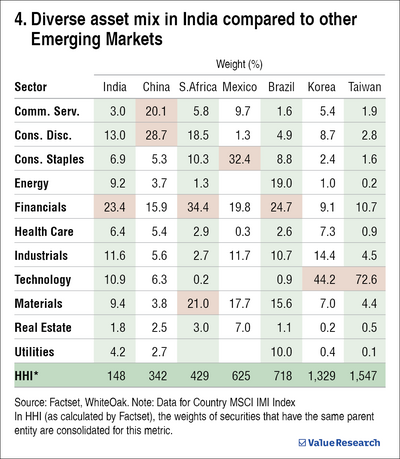

Besides state ownership, sectoral representation across various EMs is also widely different. As illustrated in Exhibit 4, compared to major EMs, the Indian market has the most heterogeneous composition at a sectoral level, and within that, it is the most diverse at the company level. For instance, Taiwan's stock market is dominated by highly cyclical tech-hardware stocks, which comprise 72 per cent of the weight, with TSMC alone accounting for 39 per cent of the total country index. South Korea is not much different, with technology comprising 44 per cent of the index and Samsung group entities across sectors forming 37 per cent of the market.

In contrast, India has the most diversified sector mix with a fair representation of most sectors. Unlike most other EMs, no single sector dominates the Indian index.

Moreover, India has a well-distributed investible universe of companies by index weights. HHI (Herfindahl-Hirschman Index) is popularly used to measure the degree of market concentration. It is calculated by summing the squared weights of the constituents. The higher the number, the greater the level of concentration. India has the lowest HHI score amongst all major EMs, evidencing the diversity or granularity of the investible universe.

Besides high concentration, sectors like tech-hardware, energy and metals & mining (which dominate many EM indices) are also deeply cyclical. Consequently, the earnings decline for commodity-intensive markets like Russia and Brazil and homogenous markets like Taiwan has been quite acute during past recessions.

On the other hand, India's diversified corporate mix entails lower exposure to cyclical sectors compared to the EM average. Consequently, as seen from Exhibit 5, India's corporate earnings have been more resilient during each cyclical downturn over the last two decades. In our view, India's relatively stable earnings profile also contributes towards its higher multiple.

In this column, we have discussed two factors - governance and quality of assets - which we believe have a significant effect on relative multiples at the aggregate country level, just as they do for individual companies. We acknowledge that many other factors influence multiples, and some might be less favourable for India.

The key message we have tried to drive home is that mere comparison of country-level multiples without adjusting for these critical factors may result in apples-to-oranges comparisons or even apples to lemons.

Chirag Patel and Manuj Jain, both CFA charterholders, are Associate Directors and Co-Heads of Product and Strategies at WhiteOak Capital Asset Management Company. They have been with the company for over two years and have over 15 years of experience in asset management. Part of the WhiteOak Capital Group, WhiteOak Capital Asset Management Company is the sponsoring entity of WhiteOak Capital Mutual Fund.

Ask Value Research ![]()