AI-generated image

AI-generated image

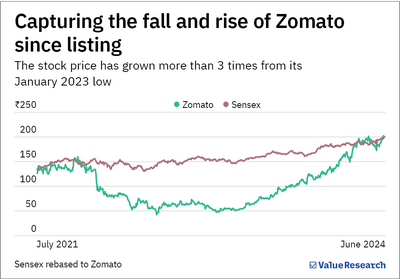

Zomato is the toast of the town, thanks to its first-ever taste of profitability in FY24. Its investors, too, couldn't have been happier. The stock has racked up a solid one-year rally of over 2 times!

Why are investors starry-eyed?

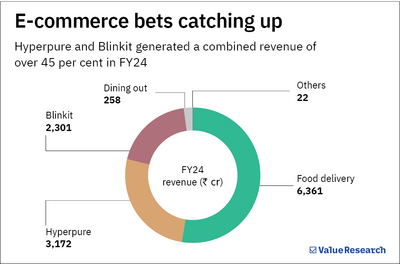

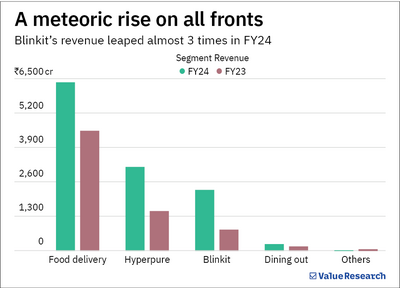

Zomato has already proved its mettle in the food delivery business, which is its primary money-spinner. The company holds leadership in this business and maintains healthy profitability. What is pulling investors in is the company's quick commerce bet that is growing leaps and bounds, beating market expectations. Zomato's e-commerce ventures-Blinkit and Hyperpure-clocked robust growth, contributing 30 per cent to the company's GOV (gross order value) in FY24. How did the company make it happen?

- Zomato added grocery delivery platform, Blinkit, to its cart in FY22 as it sought to tap the unexplored home delivery segment of household essentials, especially in metro cities. Its sharp focus on eight metro cities, scaling up of stores, and leveraging the brand name helped Blinkit grow its revenue 10 times between FY22-24. Zomato is only doubling down on the business, pegging this segment's growth at 60 per cent for FY25!

- Hyperpure is a B2B business that supplies ingredients and other kitchen provisions to restaurants. Zomato's goal has been to become an organised player in this unorganised market. The segment generates around Rs 3,000 crore in revenue currently and Zomato aims to grow it by 40 per cent in the medium term.

There's no doubt that Zomato's growth engine has finally caught steam, but what if the steam is just a sign of a slow, simmering fire? What we mean is that there remain risks that the market should not blur out as it keeps the positives in sight:

Reading between the lines

- Real profits, please stand up!

Zomato's topline, GOV and adjusted numbers are impressive, but it is not yet successful on the profitability metric. Its net profit of Rs 291 crore in FY24 is solely on account of its other income of Rs 847 crore. At the operating level, Zomato actually incurred a loss of Rs 484 crore during the year. So, its core operations remain unprofitable and cash flows only look worse.

The future guns, Blinkit and Hyperpure, are still loss-making. The management is yet to give a timeline for turning Blinkit profitable. As for Hyperpure, profitability is not even a priority at present as the business model itself is not decided. While Zomato is planning to go big on the two businesses, the gestation period for their profitability remains high, especially when the company is unsure about how long it will take to turn the duo around. Therefore, it is fair to assume that Zomato's recent profits may have just been a blip and it could easily slip into losses again, given it will keep its spending spree going for Blinkit and Hyperpure. - Competitors on its tail

While evaluating Zomato's business, the competitive heat it faces cannot be overlooked. Swiggy, the former market leader in the food delivery business, remains on Zomato's tail. Not just that, its Instamart platform is also jostling to dethrone Blinkit in the household delivery segment. Meanwhile, the Hyperpure business is yet to come up aces against the numerous unorganised players.

That said, both food delivery and quick commerce industries did not exist almost a decade ago. Zomato and Swiggy were the pioneers that broke ground in these markets, which don't have any entry barriers now. Tata's BigBasket, Amazon's Fresh, and Reliance's Jiomart are scaling up quickly in the quick commerce segment to take advantage of the vast market.

Our take

The company's recent strength is being celebrated by its backers, but the business still lacks a concrete and consistent track record of success. The business model is unique itself, which came into existence only about 10 years ago. So, there's no base or benchmark to compare it against. The industry's nature is unpredictable and the management offers loose guidance.

Despite the uncertainties, Zomato holds a higher premium than even some large, well-established businesses with superior return ratios and long-term profit scores. Considering this, it remains a risky proposition fraught with more uncertainties than prospects.

This story should not be considered as a recommendation. Investors should do their own research before making any investment decision.

Also read: This FMCG stock is eyeing high-teen volume growth. Can it ace its lofty goal?