Aanchal has benefited from a booming market. In April 2020, she had invested Rs 25,000 in equity funds which turned to Rs 39,000 by the year end. Lured by the gains, she started a Rs 5,000 monthly SIP (systematic investment plan) from January 2021.

Her Rs 2.4 lakh investment now has swollen to around Rs 3.4 lakh. While Aanchal is excited to see her investment soar, she now wonders if it is time to book profits.

Don't, unless you need the money

- Withdraw only if you need the money soon. That's because equities are unpredictable over the short term.

- However, one should withdraw in a phased manner (if invested for a non-negotiable goal) at least 12 to 18 months before you need the funds.

Don't time the market

- If you plan to re-invest the money when the market drops, don't!

- No-one can time the market successfully every time. It is also almost impossible to predict its fall. And what if the market keeps going up? You'll miss the gravy train.

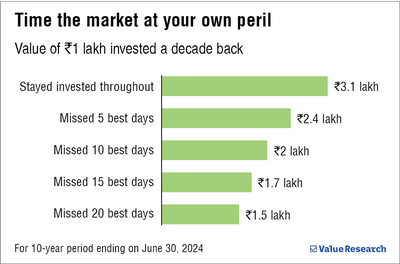

- In fact, only a handful of days are responsible for the major portion of gains from equities in the long run. Missing those days can deplete your investment's worth, as shown by the graph.

What Aanchal should do

- Asset allocation: Asset allocation helps you buy low and sell high. Here's how. Let's assume Aanchal decides on a 75:25 equity-debt allocation. If the market rises and Aanchal's equity component grows to 85 per cent, she should sell 10 per cent of her equity and invest in debt. This allows her to sell equity when they are high.

Conversely, suppose the market falls, and her equity-debt allocation becomes 70:30. In that case, Aanchal should sell 5 per cent of her debt and buy equity at a lower price to revert to the original 75:25 allocation. - Invest at least 20 per cent of your income: Invest consistently through SIPs each month, as missing them can adversely impact your long-term wealth creation.

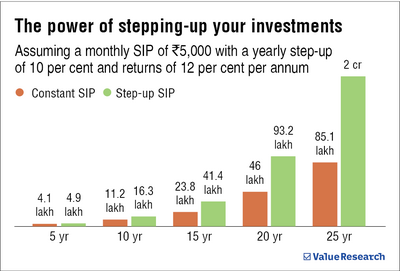

- Increase your SIP contributions: Step-up your SIPs in line with your annual increments. This can make a huge difference to your wealth.

- Invest in diversified equity funds: These include flexi-cap and multi-cap funds.

Always remember

- Equity investment should at least be for five years.

- Always invest in a phased manner. This reduces the risk of catching a market high.

- Maintain an emergency fund equivalent to at least six months of your expenses.

- Buy life insurance (term plan) if you have any financial dependents.

- Health insurance for all family members is a must.

Also read: Sky-high markets: What you should and shouldn't do