AI-generated image

AI-generated image

The idea that your portfolio should only focus on high returns is...erm...a bit flawed. Yes, earning high returns is important - maybe even the most important - but it is not the only thing that matters.

Protecting your portfolio is important, too, especially when the market is depressed. While putting all your money in equity funds may deliver high returns when the going is good, this strategy may not do so in a bear market.

Which is why you need to invest in debt funds.

Think of them as the shock absorbers of your portfolio. Debt instruments often perform better when equity markets are under stress.

While debt funds don't generate the sizzling returns we all crave, they add much-needed stability and help protect your money when the market is down and investors run out of nails to bite on. So no, these funds aren't just for retirees and boring folks - they are for every smart investor.

Ready to see why debt is important? Let's break it down.

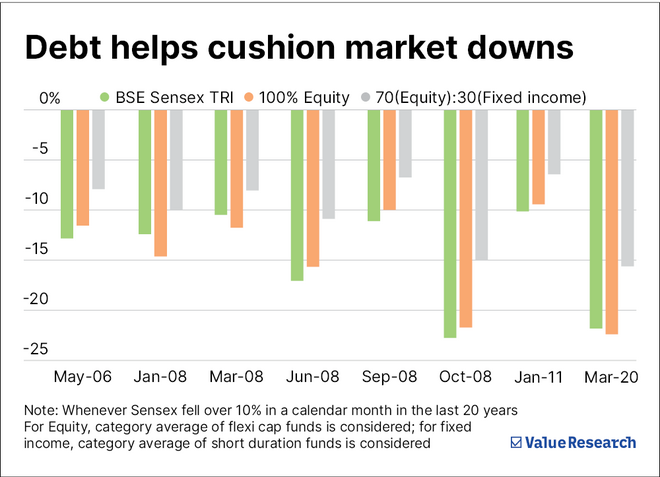

Reason 1: Debt cushions your portfolio during market crashes

Consider how a 70-30 equity-debt portfolio performed compared to a 100 per cent equity portfolio during past market crashes.

During the steep fall in October 2008, a 100 per cent equity portfolio (flexi-cap fund) declined 22.7 per cent, whereas a 70:30 mix with short-duration fixed income funds fell just 15.7 per cent.

In the Covid-led crash of March 2020, equity dropped 23.4 per cent. In comparison, the blended portfolio was down a milder 16.4 per cent.

Even during smaller corrections like in January 2008 or June 2008, the fixed income allocation consistently reduced drawdowns by 5 percentage points.

Essentially, a small allocation to fixed income doesn't just limit losses, it reduces the emotional pressure to exit your investments at the worst time. It encourages you to stay the course and reap the rewards of recovery.

Reason 2: Debt protects your non-negotiable goals

Not all goals are created equal. Some can wait—a dream vacation abroad, upgrading your car or redesigning your kitchen. But others are non-negotiable. You can't defer your child's college admission. You can't push back the day you stop working and need your retirement income to begin.

These time-bound goals demand predictability, not hope. Leaving their funding entirely to the whims of the equity market can be dangerous.

For example, imagine a parent who needed money for their child's college admission in April 2020. Back in January that year, markets were steady, and it may have seemed wise to stay fully invested in equity for a little longer. But then came the Covid crash. Between January and March 2020, the Sensex dropped over 28.3 per cent. Anyone who delayed moving to safer assets like debt would have seen a steep drop in their corpus—right before they needed it. A corpus of Rs 25 lakh at the beginning of 2020 would have reduced to just Rs 17.92 lakh by the end of March.

However, debt acts as a safeguard in such scenarios. As you get closer to achieving a non-negotiable goal, gradually shifting a portion of your portfolio into safer, more stable instruments—like short-duration funds—helps ensure your plans stay on track, regardless of what's happening in the markets.

Continuing with the above example of the person with Rs 25 lakh, if you had started gradually transferred Rs 1 lakh every month to a debt fund for the last one-and-a-half years, the same Rs 25 lakh would have gone down to just Rs 22.95 lakh at the end of March 2020, versus Rs 17.92 lakh if you hadn't.

Reason 3: Debt lets you rebalance and buy low

Rebalancing is one of the simplest but most effective investing strategies—and fixed income makes it possible.

Let's say your target allocation is 70 per cent in equity and 30 per cent in debt. If markets fall and your equity allocation shrinks to 60 per cent, rebalancing would mean you would have to shift money from debt to equity to restore your original 70 per cent allocation. In doing so, you automatically buy equity when it's down.

So, while everyone else panics, your debt allocation becomes your dry powder, ready to be deployed into equity at the most opportune time.

Stability powers smart investing

Debt may not deliver double-digit returns, but it plays a far more important role in your portfolio: protecting capital, preserving goals and empowering better decisions during uncertain times.

Your allocation to debt should be guided primarily by how far away your goals are and how much volatility you can handle along the way. For long-term goals—a 70:30 allocation between equity and debt often works well. It gives you the growth potential of equity while still cushioning your portfolio during downturns.

But as the goal draws closer, the balance should shift gradually. The nearer the goal, the more you should prioritise capital protection over return maximisation. This ensures that short-term market swings don't disrupt your plans at the last minute.

Also read: List of international mutual funds open for new investments

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()