Any profit or gain arising from transfer of capital asset held as investments are chargeable to tax under the head capital gains. The gain can be on account of short- and long-term gains. A capital gain arises only when a capital asset is transferred. Which means if the asset transferred is not a capital asset; it will not be covered under the head capital gains. Profits or gains arising in the previous year in which the transfer took place shall be considered as income of the previous year and chargeable to income tax under the head Capital Gains and the concept of indexation shall apply, if applicable.

Capital Asset: It is any property held by the income tax assessee excluding

- Any item held for a person's business or profession (stock, ready goods, raw material) will be taxed under the head profits and gains of business or profession

- Agricultural land means any land from which agricultural income is derived. Land which is not urban and is outside of 8 kilometres of a municipality, where population is less than 10,000 qualifies to be agricultural land

Capital assets are of two types: Short- and long-term capital asset.

Short-term capital asset: This is an asset that is held for not more than 36 months immediately preceding the date of its transfer. This period of 36 months is substituted to 12 months in case of certain assets like equity or preference shares held in a company, any other security listed on a recognised stock exchange of India, Units of specific equity mutual funds and Zero coupon bonds. In case of immovable property, the period of 36 months is substituted by 24 months.

Long term capital asset: This is an asset that is held for more than 36 months, 12 months or 24 months, as the case may be. Transfer is defined as the sale of the asset, giving up of rights on the asset, forceful takeover by law or maturity of the asset. Many transactions are not considered as transfer, for example, transfer of a capital asset under a will.

Stocks and units of equity diversified mutual funds qualify for long term capital gains if held for more than a year. In case of real estate, it qualifies for long term capital gains if it is held for more than two years. Earlier to the Finance Act 2017, real estate was considered as a long term capital asset only if it was held for more than three years.

Capital Gains: Any profits or gains arising from the transfer of a capital asset effected in the previous year shall be chargeable to income-tax under the head capital gains. Examples of assets are a flat or apartments, land, shares, mutual funds, gold among many others. There are two types of capital gains:

Short-term capital gain: capital gain arising on transfer of short term capital asset.

Long-term capital gain: capital gain arising on transfer of long term capital asset.

Capital gains can be taxed subject to the following conditions:

- The assessee must have owned a capital asset

- The assessee must have transferred the capital asset in the previous year.

- There must have been profit or gains as a result of such transfer

Concept of Indexation

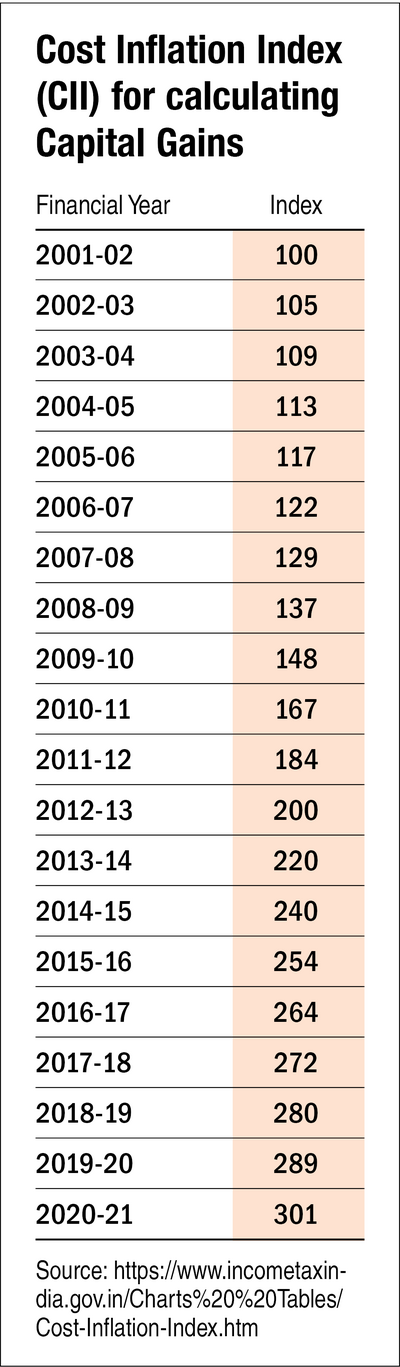

The value of a rupee today is not same as will be its value tomorrow because of inflation. Likewise to be fair when paying capital gain tax, the effect of inflation on the purchase is included. For instance if you bought a flat in January 2002 for Rs 20 lakh and sold it in January 2020 for Rs 65 lakh; you don't pay tax on the Rs 45 lakh gain. The tax authorities allow the concept of indexation so that you can show a higher purchase cost, lowering the overall profit and reducing the tax you pay on the gain. Using the inflation index, one needs to increase the purchase price of the asset to reflect inflation-adjusted true price in the year of sale. However, the benefit of indexation is available only in case of long-term capital gains.

Indexed cost of acquisition = (Cost Inflation Index (CII) for year in which asset is transferred or sold) divided by CII for year in which asset was acquired or bought). So in the above example, the year in which asset is transferred or sold is 2020-21 and the Cost Inflation Index (CII) for 2020-21 = 301. The year in which asset is acquired or bought is 2001-2002 and the Cost Inflation Index (CII) for 2001-02 = 100. So the Cost Inflation Index (CII) = 301/100 = 3.01

The CII is then multiplied with the purchase price to arrive at the indexed cost of acquisition which is the actual or true cost at the time of tax computation or calculation. The indexed cost of acquisition = Rs 20,00,000 x 3.01 = Rs 60,20,000 Hence, long term capital gain = full value of sale - indexed cost of acquisition = Rs 65,00,000 - Rs 60,20,000 = Rs 4,80,000

Tax liability on capital gain with indexation and without indexation

In case of long term capital gains, the tax liability is the lower of the amount arrived at by the two:

- 20 per cent tax liability arrived at by indexation method

- 10 per cent tax liability arrived at by without using indexation method

In the example above, using indexation, the tax liability comes to (20/100) x 4,80,000 = Rs 96,000. If you were to not use indexation: Capital gains = Sale price of asset - Cost of acquisition = 65,00,000 - 20,00,000 = Rs 45,00,000. Capital gains tax on this at 10 per cent = (10/100) x 45,00,000 = Rs 4,50,000. This is the advantage of using indexation as you benefit in saving taxes.