One section of the market that has not benefited much from the market rally is public sector undertakings (PSUs). Since April this year, when the rally started, the S&P BSE PSU index has returned 2.1 per cent. On the other hand, the Sensex has raced 35.5 per cent (as on October 27, 2020).

Historically, PSU stocks have proved to be poor wealth creators. The 10-year return of the PSU index is -7.7 per cent as against the Sensex's 7.1 per cent (as on October 27, 2020). The reasons for this dismal state of PSUs are well known: government intervention, commoditised/utility-type businesses, lack of animal spirits and their role as a vehicle for public good. Little surprise, many PSUs are trading at throwaway valuations.

But these beaten-down valuations have also paved the way for astute investors to make bets on select high-grade PSUs, which stand apart from the rest. The fundamental law of stock picking, which is to choose those companies that are likely to increase their profits, have a good track record, operate in less competitive segments yet pay a sensible price that incorporates a margin of safety, is applicable even to PSUs.

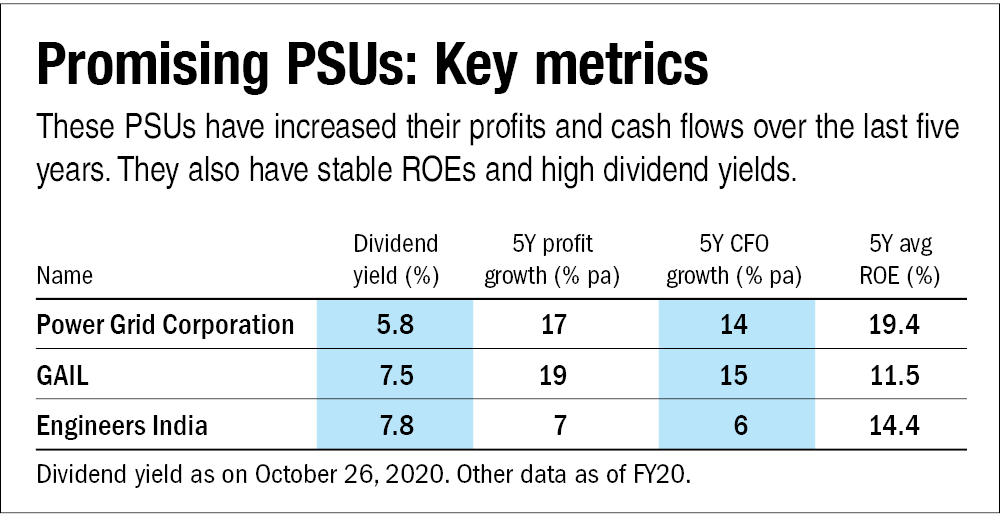

So, we have created a small list of government-owned companies that have the above-mentioned characteristics. These companies have increased their profits and operating cash flow consistently for the last five years and have a stable return on equity. And the icing on the cake is that they have a dividend yield, which is higher than the rate of bank FDs.

Power Grid Corporation of India

Operating in the electricity transmission segment-one of the most profitable segments within the electricity sector-the company owns and operates physical transmission lines that actually move electricity generated in one state to other states. These transmission lines act as the 'National Highways' for electricity and Power Grid charges a toll for allowing power generation and distribution companies to use its infrastructure.

How does it stand out?

The company's gigantic market share of 85 per cent makes it a near-monopoly in the sector. Thanks to the delayed opening-up of the private sector in the power transmission sector (which happened in 2011), the company had an unassailable head start, which no other company has been able to match. Its net profit margin of 28 per cent, which is more than four times that of its listed peer Adani Transmission is a result of its scale and long operating history.

Any headwind/tailwind?

The universal demand for electricity is unlikely to reduce in the near future, making the company almost irreplaceable. And the very likely long-term growth in the demand for its services can allow investors to sleep peacefully. But on the flip side, the sector is heavily regulated and therefore, any change in the tariffs by the regulator could easily offset an increase in the quantum of electricity transmitted.

GAIL (formerly Gas Authority of India) is a combination of two interrelated businesses. Its transmission arm, similar to Power Grid, owns the infrastructure necessary to transport a very useful source of energy. This business operates the pipelines in which natural gas is transported from ports along India's coast to different parts of the country. The company's second business is its marketing and distribution arm, which actually sells this natural gas to crores of people across the country.

How does it stand out?

The company has a very dominant status in the gas-transmission sector. And even its marketing division, which operates through subsidiaries, Indraprastha Gas Limited and Mahanagar Gas Limited, enjoys a legally protected monopoly status. The company is without peers in the transmission segment and also has a stake in Petronet LNG, which is the leading importer of LNG in the country.

Any headwind/tailwind?

Its marketing arm is facing a lot of competition from new players (including other PSUs) while attempting to expand to newer areas for which the gas regulator has recently given out licences. Given its low share in the energy basket, gas consumption is expected to increase in the country and GAIL is expected to be a prime beneficiary. Besides, the company is not affected much by fluctuations in gas prices. Any regulatory change which may reduce the prices charged by the company and any network expansion to sparsely populated areas (for example, the North-East region) could impact its profitability.

The company offers engineering services, EPC services and project implementation solutions and has become the official go-to consultant for most government/PSU mandates across various sectors, such as hydrocarbons, infrastructure etc.

How does it stand out?

The government's patronage has helped it secure many projects as the government and various PSUs have the financial wherewithal to fund large projects. Its asset-light approach and debt-free status are impressive. The company's profit margins are similar to those of L&T Technological Services, despite being a PSU. Besides, the 2800 crore cash in its bank account makes up more than half of its market capitalisation.

Any headwind/tailwind?

The company's rich operating experience is a moat in itself, which would help it if there is an uptick in infrastructure spending. However, it is highly dependent on infrastructure spending and the financial impact of the COVID-19-led pandemic on the government's finances could be a potential dampener.