At Value research, we always suggest analysing a company before investing in it. However, when it comes to analysing companies, there is no uniform set of key performance indicators (KPIs) for all companies. For example, KPIs used to analyse the performance of life-insurance companies are completely different from the ones used for other companies. In this article, we have delved into the most important parameters used to analyse life-insurance companies.

Gross written premium: An insurance company derives revenues from the total premiums it receives against the issued insurance policies. These premiums are further divided into two sub-categories - new business premiums and renewal premiums. As the name suggests, a new business premium is the premium that is due in the first year of the policy, while renewal premiums are the premiums due in the subsequent years of the policy.

Net written premium: Out of the total premium a life-insurance company receives, it pays some of this for reinsurance. Under reinsurance, an insurance company opts for insurance. More clearly, a life-insurance company insures some of its risky portfolios to reinsurers in order to diversify the risk of paying a large obligation, resulting from a high insurance claim. Basically, this is aimed at limiting the liability for specific high-risk policies during an adverse event.

Annualised premium equivalent (APE): APE is that part of the premium which pertains to the current year. We calculate this parameter because a life-insurance company gets premiums from two types of policies - regular policies and one-time payment policies. Under one-time payment insurance policies, the policyholder pays a lump-sum payment for insurance which may last many years. Thus, APE is used to normalise this one-time payment into equivalent annual payments. It is calculated by:

APE= Sum of regular annual payments + 10% of single-premium

Value of new business (VNB): It measures the profitability of new policies issued during the year. VNB is the present value of all future profits which are expected to flow to shareholders with respect to new policies written during the year.

VNB margin: It is the most important metrics to assess the profitability ratio of a life-insurance company. It is calculated by:

VNB Margin: VNB divided by APE

Embedded value: Unlike VNB which pertains to the current year, embedded value is the consolidated value of shareholders' interest in the company. It measures the value of a life-insurance company to its shareholders. Thus, VNB is simply the increase in embedded value during the year.

Embedded Value: Present value of future profits + net asset value of the company.

Assets under management: It is the carrying value of all the investments of a life-insurance company.

Persistency ratio: It measures how long customers continue their policies. It is depicted as the percentage of policies that have not lapsed and is mostly expressed at a frequency of 13th month (second year) and 49th month (fifth year) following the issuance of the policy. For example, a 61st month persistency ratio of 40 per cent means 60 per cent of the policyholders are not paying premiums and only 40 per cent of the policyholders are paying premiums even after five years. It measures the association of customers with the company. A longer duration is better for the company.

Claim-settlement ratio: This is the total number of claims paid out against the number of claims filed by policyholders of the insurance company.

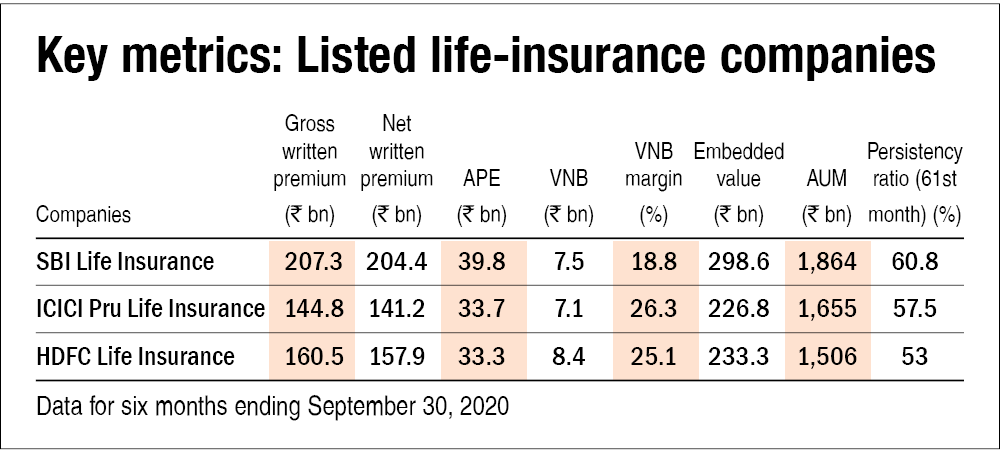

Let us now look at the key parameters for all the listed life-insurance companies: