After becoming proficient in reading the cash flow from operations, it is now time for investors to understand the second part of the statement of cash flows, i.e., the cash flow from investments. This part is present between the cash flow from operations and the cash flow from financing.

What is it?

The cash flow from investments is a simple statement that conveys to the reader information regarding how an entity has utilised its cash resources for investment-related activities. In the context of the cash flow from investing, investment activities refer to buying and selling long-term assets such as factories, equipment, shares, and fixed deposits (FDs). Only transactions that result in a recognised asset in the balance sheet are eligible for classification as investing activities. The sum of all the gross cash flows from investing gives the reader the Net Cash from Investing, which can either be a positive number or a negative number. While a positive value represents a cash inflow, a negative value indicates a cash outflow. A key point to note is that investing activities represent money invested by the company, and any money invested in the company is classified as a financing activity.

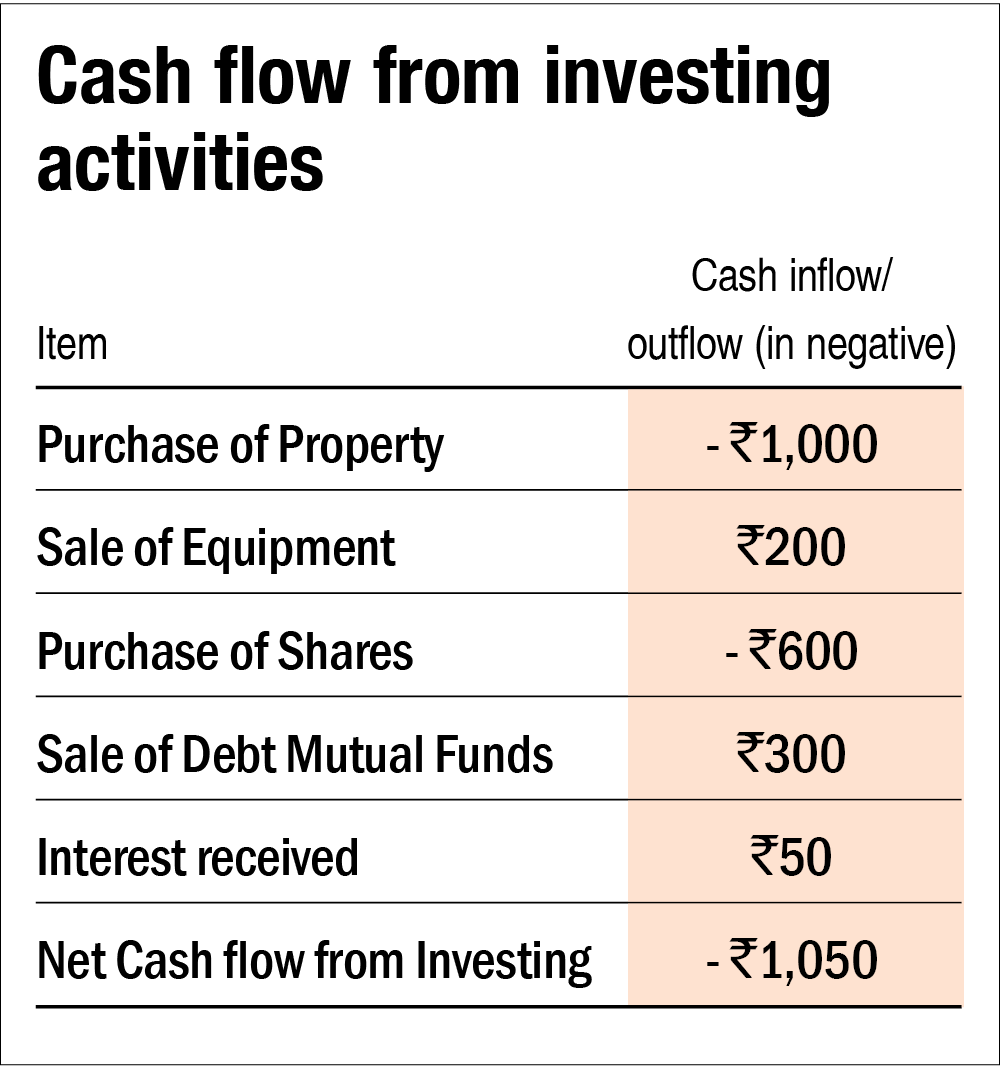

An illustration of a hypothetical company's cash flow from investments would look like this:

Why is it important?

A company will need to spend money on equipment, buildings, land, etc., to grow or maintain its business. And during the course of its business, it may sell these assets (when they are outdated) and continue to invest in new assets. By giving readers a good understanding of both the nature and the quantum of investments undertaken by the company in different asset classes, cash flow from investments is useful in assessing the future potential of the company's operations and anticipated changes, if any.

For example, a mature company may not invest in new assets. In contrast, a young company may decide to go on an investment binge to increase its capacity or expand to new markets. This information could give investors a reasonable expectation that while the young company's revenue may go up in the future, it is likely to remain stagnant for the mature company.

Exceptions

Despite the cash flow from investments having just one method of preparation, unlike the cash flow from operations (which can be prepared using two methods, i.e., Direct and Indirect Method), certain tricky aspects have to be kept in mind.

One, all investments in instruments held for trading purposes or considered 'cash equivalents' are not included in the cash flow from investments. These instruments are not counted for investment purposes since cash equivalents are primarily held to meet short-term commitments, and trading is usually considered an operating activity.

Two, the classification of interest and dividend payments would depend on the nature of the underlying business of the entity. If the entity is a financial institution, such transactions would be captured in the cash flow from operations, but for other entities, these transactions will form a part of the cash flow from investing activities.

Three, if investors are looking at foreign companies, they have to be mindful of the subtle distinctions between international accounting rules and domestic accounting rules (IFRS vs Ind AS is a separate topic altogether).

Conclusion

The cash flow from investments is useful for many purposes. You can use it to comprehend the sources of investment cash flows, understand the business's long-term investment requirements, and predict future cash flows. Given that the cash flow from investments also provides information regarding interest income and dividend income, it can be used to assess the performance of unlisted subsidiaries and other investee companies.

And when used in conjunction with the profit and loss statement and operating cash flows, cash flow from investments aids investors in better appreciating the financial affairs of a company. And to state the obvious, investors must always ensure that they look carefully at the cash flow statements before making any investment decisions. All the information regarding the cash flow statement of every domestic listed company is freely accessible on Value Research Online, and details are available under the 'Financials' tab.

Also in the series: