There are three categories of residents in India under the Income-tax Act - resident, resident but not ordinarily resident and non-resident depending on the number of days spent in India.1 A similar but not identical definition is laid down in the Foreign Exchange Management Act (FEMA). Special rules on bank accounts, investments and taxation have been laid down for non-resident Indians.

Bank accounts

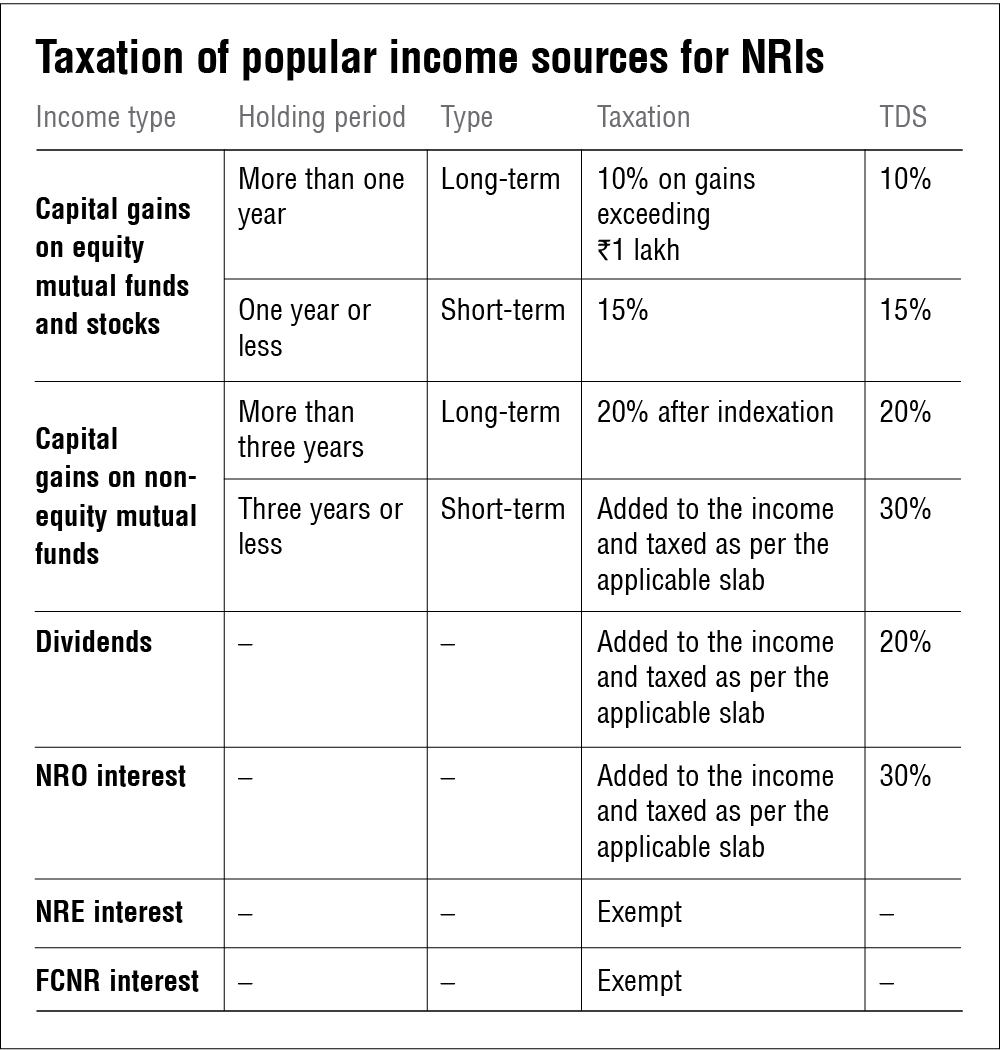

Non-resident ordinary (NRO) account

This is a rupee-denominated savings bank account for non-resident Indians. It is a non-repatriable account, meaning that the money in this account cannot be transferred outside India by its holder. Interest on this account is added to the income of the NRI and taxed like other income. They can also create Fixed Deposits (FDs) from the balance in the NRO account. The interest from such deposits is taxable. They can transfer money from the NRO account to the NRE account by obtaining the 15 CA/CB certificate from a chartered accountant that applicable taxes on the amount being transferred have been paid.

Non-resident external (NRE) account

This is a rupee-denominated savings bank account geared towards holding the foreign earnings of NRIs. Its interest is not taxable in India and its balance is fully repatriable (transferable) outside India. They can also create Fixed Deposits (FDs) from the balance in the NRE account and the interest thereon is exempt from tax. Premature termination of an NRE deposit before the passage of one year will lead to forfeiture of all interests on the deposit.

FCNR account

This is a foreign currency fixed deposit available to NRIs. The interest on this account is exempt from tax and the balance in the account is fully repatriable outside India. Premature termination of an FCNR deposit before the passage of one year will lead to the forfeiture of all interests on the deposit.

(1) He is in India for a period of 182 days or more in that year; or

(2) He is in India for a period of 60 days or more in the year and for a period of 365 days or more in 4 years immediately preceding the relevant year.

However, if an individual leaves India for the purpose of employment, business or any other purpose without the intention of returning in a certain period, only condition (1) is applicable. Budget 2020 amended this rule for Indian citizens earning more than Rs 15 lakh in a relevant year from Indian sources. For them, both conditions are applicable and the limit of 60 days is to be taken as 120 days.

Also, Indian citizens earning more than Rs 15 lakh in a relevant year from Indian sources and who don't have a domicile or residence in any other country will be deemed to be Resident of India.

Resident but not ordinarily resident: Under the Income-tax Act, 1961, an individual is a resident but not ordinarily resident if he fails to satisfy either of the following conditions: (1) He is resident in India for at least 2 years out of 10 years immediately preceding the relevant year; (2) His stay in India is for 730 days or more during 7 years immediately preceding the relevant year.

Also, as per Finance Act 2020, an Indian citizen who earns more than Rs 15 lakh from Indian sources and has stayed for 120 days or more but less than 182 days during the relevant year is a not ordinarily resident.

Also read: Mutual fund investments for NRIs