Sale and discount - two words that are enough to lure in any buyer. And the stock market is no different.

No, we are not saying that you should avoid stocks trading at a discount. Rather, we at Value Research have always stated that purchasing fundamentally strong businesses when they have fallen out of the market's favour is a core tenet of long-term wealth building.

However, blinding following valuation metrics without considering other factors can be disastrous for your portfolio.

Take the example of price-to-book value (a valuation metric). Book value represents the amount that would be left for shareholders if a company sells all its assets and clears all its liabilities. In simpler terms, it represents the net worth of the company.

Price-to-book value signifies the price multiple the market has assigned to a company's book value. So, if a company is trading at a price-to-book value of two, it means the company is available for two times its net worth.

Thus, when a company has a price-to-book value of less than one, it means investors can purchase the business at a price lower than its net worth. Unsurprisingly, such a lucrative offer draws in a flock of buyers.

But does it guarantee returns? After all, unlike your other purchases, the primary goal of purchasing a stock is returns.

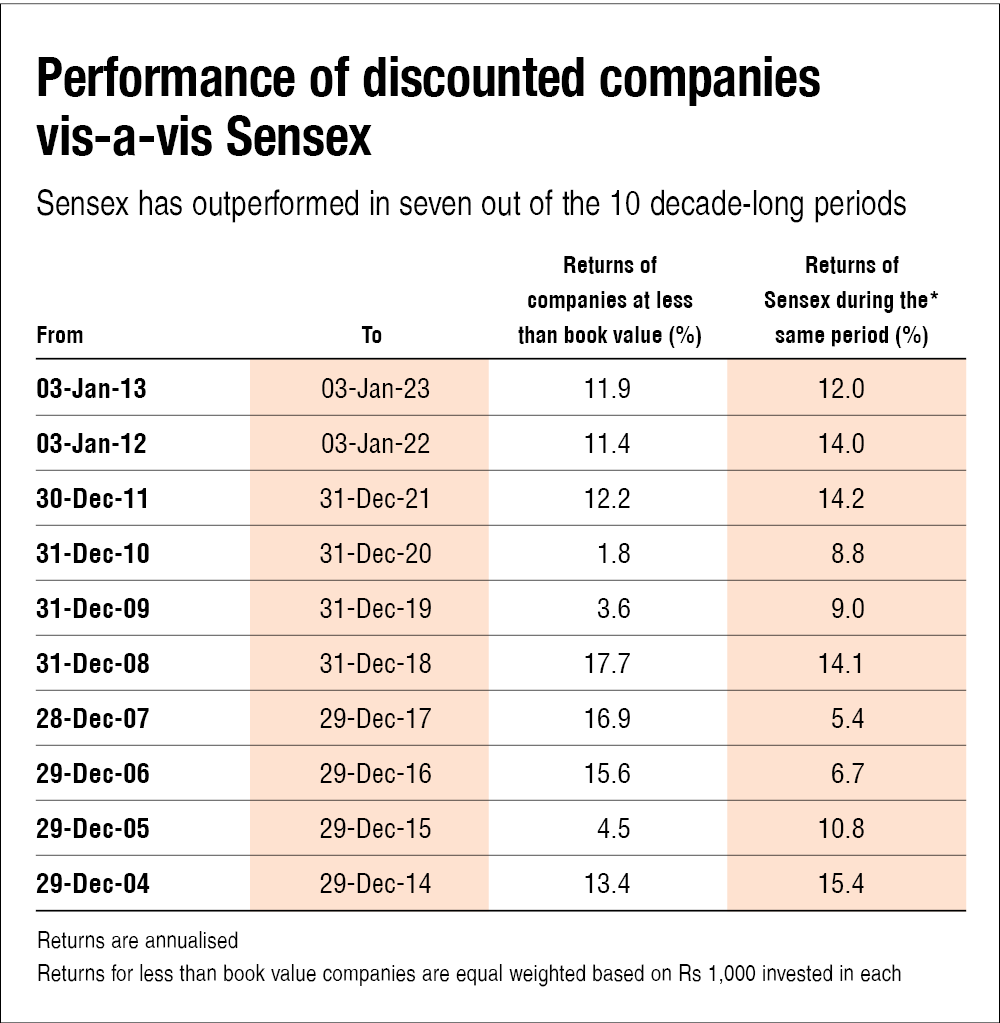

To explore if investing purely based on price-to-book value is actually rewarding, we did the following exercise. We picked the top ten stocks in terms of market capitalisation that were trading at a price-to-book value of less than one at a certain point in the past. Next, we evaluated how much returns they would have given in 10 years. We conducted this exercise for 10 decade-long periods. For example, we took all the companies that traded at a price-to-book value of less than one on January 3, 2013, and estimated how much returns they would have given if one remained invested for ten years after purchasing them at that price.

As you can see, Sensex outperformed these companies in most cases. In short, if you had a portfolio comprising only stocks that were trading at a low price-to-book value during the above periods, you probably wouldn't have beaten the overall market.

In addition, even during the few years our hypothetical portfolio beat the market, such as 2007 to 2017 and 2006 to 2016, it was mainly thanks to one or two stocks performing well. For example, in the 2007 to 2017 period, the average return of our ten selected stocks was a measly 7.9 per cent. However, Whirpool India's and Vardhman Textile's superior performance saved the day.

An intriguing coincidence?

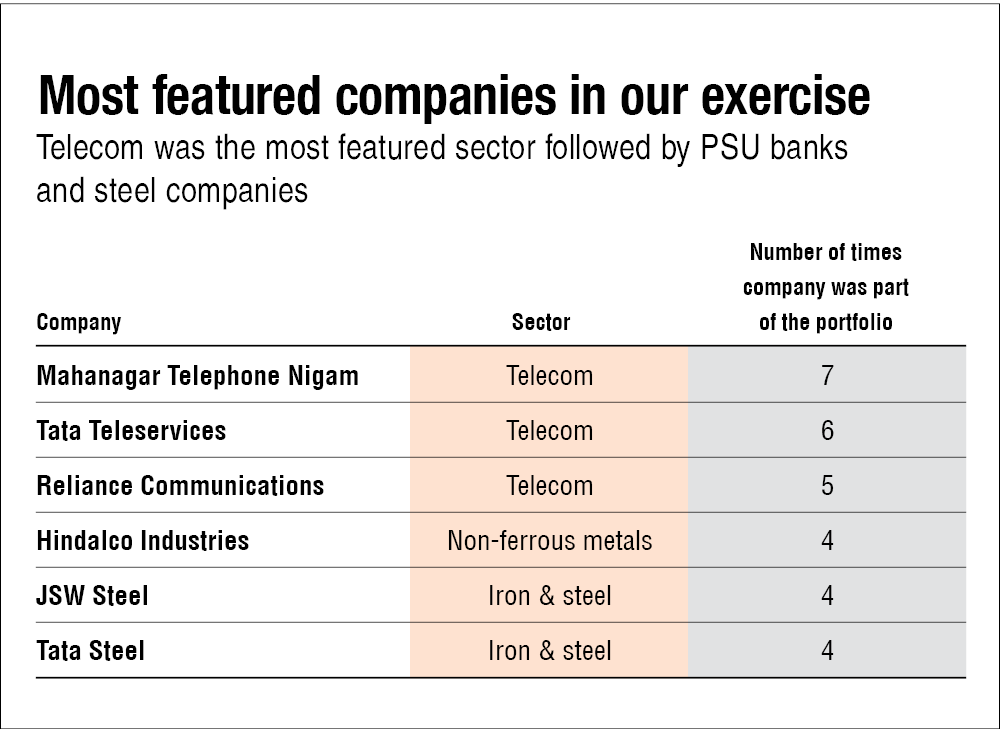

Another thing we uncovered in our exercise is that cyclical companies regularly trade at a price-to-book of less than one. We all know the risks that we get from cyclical stocks despite how attractive they may look.

These are the companies that featured most often in our exercise.

So are we saying never purchase stocks that are trading at a price to book of less than one?

No, of course not.

The purpose of our exercise was to show that blinding following discounts in the stock market might not be the best move. Indeed, a cheap valuation should always intrigue you to look into a business. However, as always, how good a business is, how good the management is, its past performance, and its future outlook should take precedence over its price.

Undervalued stocks can often be rewarding, but it is necessary to check if the discount is based on the market ignoring some factors or if it is just a bad investment.

Suggested read: Negative working capital is not always negative