SEBI recently initiated a study of existing fees and expenses charged by mutual fund houses. While AMC bosses usually view such initiatives as another exercise in trimming expense ratios, I think SEBI should look at two other urgent issues that need fixing.

First is that AMCs are paying higher commissions for newer funds, potentially creating incentives for distributors to churn investors' money, a malpractice SEBI has worked hard to discourage over the years.

Second, higher commissions of new funds have led to exceptionally low expense ratios for their direct plans. While it may be a blessing for now, it will eventually impact direct plan investors negatively once AMCs stop promoting these funds aggressively and reduce the commissions.

Both these matters have significant implications for you, the investor, and therefore must not be ignored.

Need for SEBI scrutiny

Before examining these issues more closely, let's begin with a more fundamental question: is SEBI really unfair in its unrelenting focus on costs? Well, even if the expense ratio is over-regulated, I think that's how it should be. While you normally expect market forces to take care of prices in a competitive and transparent industry, mutual funds, particularly equity funds, are a strange beast. Performance in this industry is such a big driver that if a fund does well, expenses don't matter - even if they are on the higher side. Conversely, if a fund doesn't do well, even lower expenses wouldn't count much. Therefore, the need for regulatory intervention to protect investors.

Without a tight regulatory leash, mutual funds could have easily gone the PMS or ULIP way. Do you remember they would charge as high as 6 per cent in the name of initial-issue expenses to launch a new fund? 6 per cent! If not for SEBI's heavy crackdown, the mutual fund industry would have been happily fleecing you to this day.

From abolition of initial-issue expenses to ban on entry loads to setting expense-ratio limits, SEBI has had to take several measures to ensure mutual funds are one of the most cost-effective investment products. But despite these reforms, grey areas remain.

Distributing fairness

The biggest issue is to get distributors aligned with your interest. The presence of the entry load - which encouraged distributors to ensure we kept hopping from one fund to another to line their own pockets - was a sore point until SEBI intervened. But the scars are not gone yet. Now, AMCs offer distributors a higher percentage of trail commission for their new funds - a simple case of sour wine in a new bottle.

To illustrate my point, the newer actively managed equity funds (launched in 2020 or later) are paying an average of 1.65 per cent of AUM to distributors as commission, while the ones launched before 2020 are paying around 1.10 per cent. This means a distributor earns about 50 per cent more by selling new funds to you. This structure potentially incentivises unnecessary fund churn, which is debilitating for us in the long run. This issue needs fixing.

The cost of being direct

The second issue is how the expense ratio of a direct plan is calculated. Currently, you subtract distributor commission from the expense ratio of the regular plan to arrive at the number. But I feel this is a flawed configuration because agents' commissions should have no bearing on direct-plan expenses. Isn't that the point of investing in a direct fund? Moreover, since distributor commissions vary widely from fund to fund (as discussed above), why should direct-plan investors be affected by them?

Ideally, the rise and fall in distributors' commission should impact the expenses of regular-plan investors only. After all, they are the ones being served by distributors. So, if an AMC pays lower commissions, investors of regular funds should benefit from it. And if they pay higher commissions, regular funds' expenses should be affected. In all of this, the expense ratio of direct plans should remain unchanged.

But in reality, expense ratios of regular plans remain sticky at the top end of what's permissible by SEBI, while any fall in distributor commission increases the expenses of direct plans and vice versa. This needs to change. Mind you, the issue is not so much about the quantum of direct-plan expenses at this point but about the way they are calculated. There are plenty of new funds launched in recent years that are paying handsome commissions, making direct plans look cheap right now. But going forward, (if and) when these fund houses reduce commissions, the expense ratio of direct plans will increase, hurting the interests of 'direct' investors.

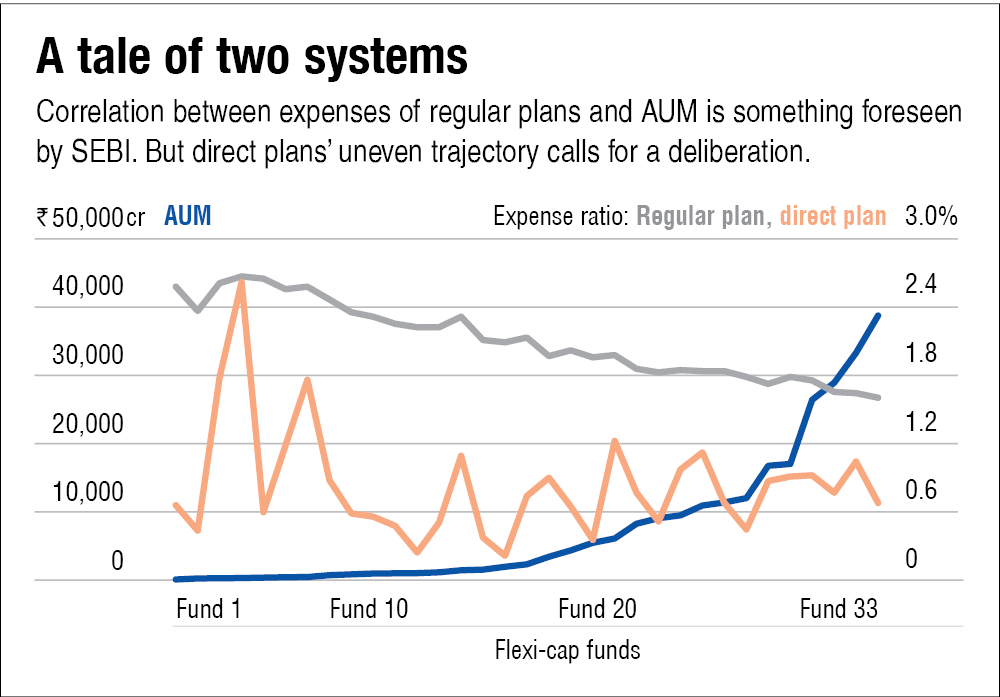

See the graph A tale of two systems, which maps the AUM and expense ratios of all flexi-cap funds (Fund 1 being the smallest flexi-cap fund by AUM and Fund 33 being the largest). In the case of regular plans, you can see the expense ratio progressively reducing with an increase in fund size. This is exactly what SEBI intended to achieve with its tiered expense-ratio formula for regular funds.

But in the case of direct plans, the expense ratios are quite random. Direct plans of AMCs which pay big distributor commissions tend to be exceptionally cheap, while those that pay less seem to be more expensive, irrespective of the AUM.

Ideally, it should be the other way around. The expense ratio of direct plans should be more sticky and progressively fall with the rise in the AUM. Regular plans, meanwhile, should rise and fall depending on the AMC's commission structure.

This is why SEBI should introduce a tiered system of expense ratios for direct plans (with much lower slabs, of course) and a broad framework for distributor commissions. Once these are in effect, expense ratios of regular plans would automatically fall in place. While this method may make direct plans of some funds more expensive, I believe the system will be a lot fairer.

In summary, SEBI has done a tremendous job moderating the expenses of mutual funds over the years. But its two other important goals of disincentivising churn and keeping direct plans immune to distribution commissions remain partially fulfilled. More than tightening the screws on costs further, it should focus on these issues in its latest study.

This story first appeared in the February 2023 issue of Mutual Fund Insight.

Suggested read: How does expense ratio affect returns?