The world is changing. So is India.

We're in an era of growth. And never before in the history of finance and economics have women been more instrumental. While women are increasingly taking charge of their finances, they are still far behind where they can be.

So, let's see how our women can invest and grow their money better.

Myths around women and money

One of the common reasons why many women shy away from investing is the number of myths surrounding women and finance.

The biggest of them is that women do not understand finance or do not have the mathematical abilities needed to make the right decisions. Another myth is that women are not good at managing money and they are risk-averse.

On top of everything else, the belief that women love to splurge is one thing that makes many people believe that women do not make good investors.

What's the truth

A lot of these myths, in reality, are simple gender biases. One doesn't need a lot of background in Maths and Statistics to make wise financial decisions.

Although there is no research available in India, some reports from the developed economies suggest that women end up spending more on essential family needs like food, clothing, medical expenses etc. This leads to lower surplus investable income with them, hence the myth that they spend more.

And yet, despite the conservative household budgets, our women, through generations, have been managing to save money. All that needs to change for women to generate wealth is to put this money in suitable instruments.

Financial decisions are not rocket science. Common sense is as instrumental to finance as any other decision-making process, and women have it in plenty and then some. As far as the more technical aspects of investing are concerned, there's always expert advice available, just like it is for men.

How is the scenario changing

For women to be in charge of their wealth, the game has to change on multiple levels. Change has already begun and is visible to an extent.

For instance, at the national level, India's recent economic growth has been nothing short of a perfect winning-against-all-odds script. Organisations like the IMF and the World Bank are raving about India's resilience even in the currently chaotic world.

This means more opportunities for women to invest.

On the other hand, the push behind women's entrepreneurship, STEM education, diversity and inclusion at workplaces, and women's safety, has enabled them to earn more.

Aprajita Anushree

Aprajita Anushree

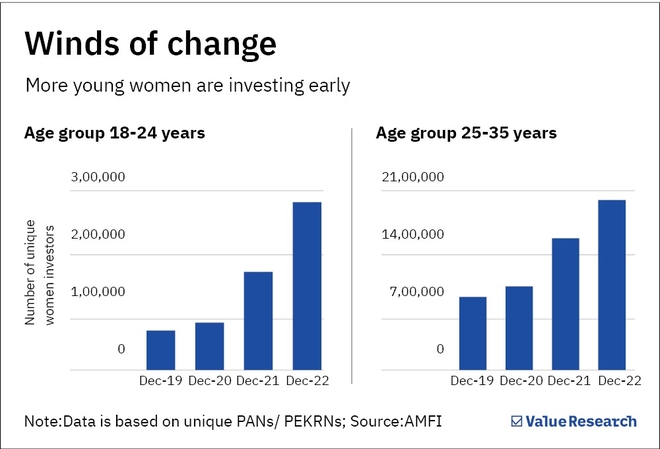

The latest AMFI data indicates that the number of women between 18 and 24 who invest in mutual funds has grown more than four times (62 per cent annualised growth) from December 2019 to December 2022.

Similarly, the number of women investors in the 25-35 age bracket has doubled (grew at 33 per cent) over a similar period. In contrast, the older age groups have grown relatively slowly, at 11 per cent annualised growth.

Aprajita Anushree

Aprajita Anushree

How to start your investment journey

If you still haven't started investing, our first advice is to begin. There is no better time to invest than now. So, just start.

Also, do not hesitate to seek expert advice or professional support when choosing the right investment instruments, specially in the early stages of your journey.

Remember, the basic principles of investing and the larger economic framework of the country remain the same for men and women. So, any piece of advice on investment remains as valid for your investment journey as it is for your male counterparts.

However, here are some simple steps summarised to start your journey.

- Start investing with discipline. You can start an SIP with as less as Rs 500, and do your KYC and payments online.

- Stay regular. Don't lose tempo, get bored, or forget to keep investing.

- The next step in investment is to plan your goals. Your goals can be either short-term or long-term. For instance, retirement is a long-term goal, while buying a car can be a short-term goal. In a long-term horizon, you invest regularly for five years or more. A short-term investment horizon is one to three years.

- Choose the right fund. This critical step may look complicated, but this is no rocket science.

- A debt fund is a good choice if you're investing for a short-term goal. For any long-term goal, an equity fund is the best option. It balances your risk and returns well.

- If you're a first-time investor in an equity fund, you will initially benefit from an aggressive-hybrid fund. It reduces your risk and lets you witness the value of systematic investing over two to three years.

- Once you get a hang of the market, you can quickly move to pure equity funds, say a flexi-cap fund, for good returns.

- Increase your SIP gradually. If you're a working woman, keep increasing your SIP as your earnings increase. If you're a homemaker, you can still invest an extra amount whenever you get cash gifts, inheritance etc.

- Remember, your key to success is the consistency of investment so that you can create an emergency corpus or a nest egg for your old age.

The message is simple.

The fundamentals are not gendered. So, your journey doesn't have to be stereotyped, either. Women can manage finances; they do manage finance. And successfully so.

The other key principle to note is that there's saving, and there's investment. And, if you want to grow your wealth, you must begin investing now.

India is on the cusp of something great. The next 25 years are expected to make the country reap the magical benefits of the last 75 years of effort. And there's no reason why women should not benefit from this golden period!

Suggested read: Women and finance