Arbitrage funds were hit with a wrecking ball in the previous financial year. They got hammered - like, erm, Aamir Khan's Thugs of Hindostan did at the Box Office - witnessing net outflows of a little over Rs 35,000 crore, almost a third of the assets they were managing.

But what a difference a (financial) year makes.

Fast-forward to now, they have become bonafide superstars, receiving net inflows of nearly Rs 49,000 crore in just seven months (April 2023 to October 2023).

But how did they transform so astonishingly?

Taxation

Blame it on debt funds losing indexation benefits . Indexation, basically, reduced capital gains tax because it took inflation into account.

If you are wondering what the big deal indexation is, here's an example:

Say, you invested Rs 2 lakh in April 2017. In 2023, the money increases to Rs 3 lakh.

Without indexation, the gain of Rs 1 lakh would be added to your income and taxed accordingly. Assuming you are in the 30 per cent tax bracket, you would have to pay Rs 30,000 tax.

But with indexation, your investment would be adjusted for inflation and then be taxed at 20 per cent, which would be Rs 8,824.

Returning to arbitrage funds, they are treated like equity-oriented funds, which enjoy superior taxation. With these funds, you end up paying a 15 per cent tax on short-term capital gains and a 10 per cent tax on long-term gains, only if they exceed a lakh of rupees in a financial year.

In addition to being more tax efficient, arbitrage funds can be risk-free, too. Let's explain why.

How arbitrage funds make money

As the name suggests, these funds invest in arbitrage opportunities. For instance, if the shares of a company trade at Rs 100 on NSE and Rs 105 on BSE, the fund would buy the stock at NSE and sell it at BSE for a profit of Rs 5.

Similarly, there can be a price difference between the cash and derivatives markets. Let's say a company's share price is Rs 104 in the cash market, and its Futures contract trades at Rs 115; the fund would buy the shares and sell the Futures.

Since they are less volatile compared to a regular equity fund, a lot of investors are parking their emergency money in them instead of liquid funds.

Arbitrage funds vs liquid funds

If you are a Value Research reader, you'd know that we recommend liquid funds to keep your emergency money since they are safe.

That said, arbitrage funds have delivered healthier post-tax returns.

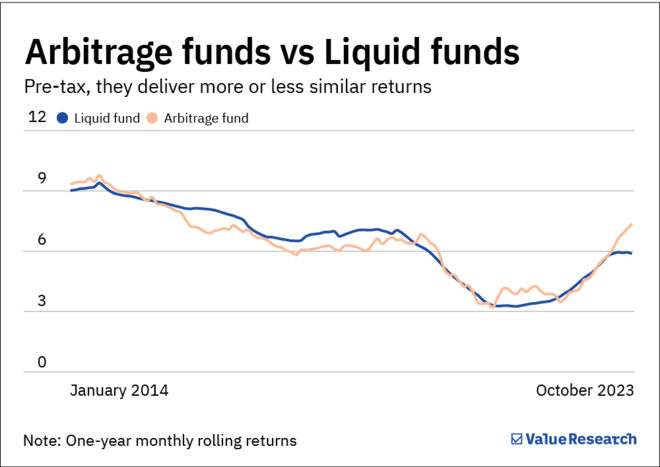

If you look at the one-year pre-tax returns of the two, they are pretty much even-stevens. But it is the post-tax returns that favour arbitrage funds (see the graph below).

So far, so good.

But, in terms of its risk profile, liquid funds are safe and less volatile, even when you compare them with arbitrage funds.

Since many people view arbitrage funds as an alternative to liquid funds for parking your idle money, let's look at the worst outcomes over different short-term horizons.

As bad as it gets

Worst returns over short term horizons (in %)

| 1-month | 3-month | 6-month | 12-month | |

|---|---|---|---|---|

| Arbitrage fund | -0.22 | 0.12 | 1.35 | 3.09 |

| Liquid fund | 0.2 | 0.76 | 1.57 | 3.24 |

| Note: Based on 1- , 3- , 6- and 12-month rolling returns (pre-tax) of the category average since 2013. | ||||

Our take

Given their relative volatility, does it make sense to invest in them?

That depends on three factors:

-

How much idle money you have

-

Which tax bracket you fall under

- Your risk profile

Here's why: If you look at the table below, arbitrage funds would help you earn 0.6 to 1.5 per cent more than liquid funds. But the difference would only be substantial and meaningful if you have a sizable amount of idle money, b) fall in the 30 per cent tax bracket and c) can stomach short-term volatility.

The investment case for arbitrage funds

These funds suit those who have a sizable amount of idle money and fall in the 30 per cent tax bracket

| Investment amount (in Rs) | Higher post-tax returns vs liquid funds (short-term) (in Rs) | Higher post-tax returns vs liquid funds (long-term) (in Rs) |

|---|---|---|

| 10 lakh | 6102 | 15615 |

| 25 lakh | 15255 | 33182 |

| 50 lakh | 30510 | 56364 |

| 75 lakh | 45765 | 79546 |

| 1 crore | 61020 | 102728 |

| 2 crore | 122040 | 195457 |

| Note: Average 1-year rolling returns of the respective category averages have been used. In case of long-term gains, it is assumed there are no other gains to be adjusted against the Rs 1 lakh limit. | ||

If you don't tick these boxes, your money can seek refuge in a liquid fund.

Also read: Are battered arbitrage funds on the road to recovery?