As cliche as it may sound, change is the only constant in life. From the innocence of childhood to wisdom of age, our life is in a perpetual state of change. So, if we know there's a gradual shift in our perspectives and beliefs over time, why should we not extend that same courtesy to our investments?

To this day, most Indian households swear by bank deposits and Public Provident Funds (PPFs). Our parents still wax lyrical about these two investments. They are like family heirlooms, passed down generations. The numbers bear this point, too. As per the Reserve Bank of India, over 48 per cent of Indian household's financial investments lie in bank deposits and PPF as of March 31, 2023.

'Lie' is the operative word here. 'Lie' because even though, like our lives, the world of investments has changed, we have refused to move on with time, refused to see that these old warhorses are nothing but a relic of the past, especially when compared with mutual funds.

Performance

True, PPF still retains some merit, especially for conservative investors or those looking for 'low risk-low return' options, but have you heard of flexi-cap funds, a type of mutual funds that can invest in companies of various sizes? Did you know these funds can be a good option for long-term investors?

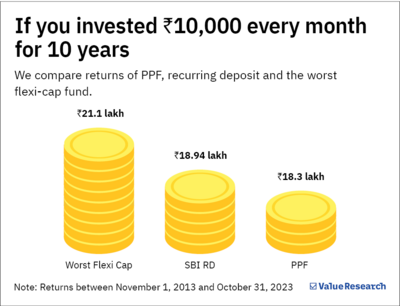

If you do, you should know that an SIP even in the worst flexi-cap fund of the last 10 years has out-flexed the two veterans. Between November 1, 2013 and October 31, 2023, the biggest dud among the flexi-caps delivered 10.36 per cent compared to SBI recurring deposit's 8.5 per cent and PPF's 7.86 per cent!

To give you added perspective, a Rs 10,000 monthly investment in a flexi-cap fund would have grown to Rs 21.1 lakh at the end of 10 years, while the bank deposit and PPF would only reach Rs 18.95 lakh and Rs 18.27 lakh, respectively.

Post-tax returns

Even if you consider tax, the dullest flexi-cap would still come out on top despite PPF offering tax-free returns.

The post-tax returns are even worse for recurring deposits because the interest earned is added to your taxable income and taxed as per applicable slab. It means that for someone in the highest tax-bracket, the interest will be taxed at 30 per cent as against capital gains tax of 10 per cent in case of a flexi-cap fund.

Our take

- Despite the PPF being a secure and tax-friendly option, flexi-cap funds can be an investment choice for long-term investors with a moderate appetite for market fluctuations.

- Forget the worst-performing fund, a closer examination reveals that 63 per cent of flexi-cap funds gave more than 14 per cent returns over the last 10 years. This means that you should not fall into a state of analysis paralysis while trying to select the right flexi-cap fund. As the numbers attest, even investing in a so-called incorrect fund can be better than not investing in one or being stuck in the past.

Also read: The high road vs the low