STP may be to SIP what Brazil's Garrincha was to Pele. While the world knows all too well about the genius of Pele, the winner of three football world cups, few outside Brazil remember the brilliance of Garrincha, the architect of Brazil's 1962 World Cup win. Only a handful can recall that Pele hardly kicked a ball in that edition (he got injured early in the tournament) and that it was Garrincha who inspired the Seleção, as the Brazil team is popularly known, to win that World Cup.

Likewise, while everyone knows about SIPs (systematic investment plans) and that SIPs are 'sahi hai', few investors are aware of STPs (systematic transfer plans). But the irony is that even if you call STPs the poor cousins of SIPs (at least in terms of their popularity), they can make you more money, especially if you have a lumpsum of money on hand.

Let's explain how.

Equity markets are known to be incredibly moody over the short term, making it less than ideal for you to put your money in the market in one shot. If you do so, your money will go up and down every second, causing you to panic if you are a relatively new investor.

Hence, the better option while investing in an equity fund is to spread your investment over a few months or years, depending on how large the corpus is and how significant the money is to you. The larger the corpus and the higher its significance, the longer should be the time across which the investment should be spread. Because you wouldn't want to invest, say, Rs 5 lakh in the market in one go and then see the money oscillate wildly with each market fluctuation. Instead, spreading the Rs 5 lakh over a year would reduce the risk of sleepless nights and timing the market.

The rest of the money, meanwhile, can be kept in your bank account. OR MAYBE NOT.

Here's why: A savings account of a prominent bank usually delivers around 3 per cent interest, much lower than the average inflation rate of the last decade. That means the money lying in your account is actually rotting.

The better option

Stick to your original plan of spreading your money. It will help you stave off the market's short-term ups and downs.

However, instead of keeping the idle money in a bank account, stash it away in either of these two debt fund options:

For one, both these debt funds can provide higher returns than a bank savings account. For instance, the one-year return of both an average liquid and an ultra-short-duration fund ranges from 6.5 to 7 per cent. In contrast, a reputed bank offers 3-3.5 per cent for keeping the money in their savings account.

What's more, these funds can deliver even higher returns in the next few months, as interest rates are at their peak in India. For the uninitiated, since the Reserve Bank of India is unlikely to raise the interest rates any further, investors stand to gain more because when rates fall, debt funds generate higher yields.

Moreover, both options are reasonably safe and liquid, meaning you can withdraw your money at short notice.

Third, there's a risk of spending your money in your bank, whereas keeping your money in either a liquid fund or an ultra-short duration fund can instil discipline.

Now that you know why keeping your money in either of these debt funds is better, let us explain where STP comes in.

Introducing STP

If you are looking at practicality, transferring money from either of the two funds to an equity-oriented fund each month can sound tedious.

Hence, the need to start an STP (systematic transfer plan). This facility can transfer your money from one fund to another.

Just like SIPs help you transfer money from your bank account to a mutual fund, STPs transfer money from one mutual fund to another.

STP vs SIP

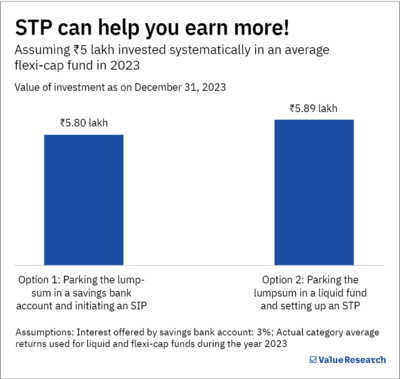

Remember we told you STPs can make you more money? Let's show you how.

Look at the graph. You'll see that the STP option would have helped you earn Rs 9,000 more last year alone. Since STPs enable you to hold your money in a liquid or an ultra-short duration fund, your money would earn higher returns than if you had kept it in a bank account.

That said, there are a couple of drawbacks.

An STP is only allowed if the two funds belong to the same fund house. For instance, if you want to invest in Parag Parikh Flexi Cap Fund, you'll have to invest in a Parag Parikh's debt fund to start an STP.

Also, interest of up to Rs 10,000 from a savings account is not liable to taxes. But even if you consider this, the potential of earning higher returns through an STP can outweigh the tax benefits of a savings account.

The rest of the taxation bit is the same. The interest or return is added to your annual income and then taxed as per your tax slab.

Our take

Start an STP instead of an SIP if you have a lumpsum amount.

STPs will help you make more money because they allow you to shift your money from a low-earning savings account to a liquid or an ultra-short duration fund.

Also read: What's best for STP?