"You say the economy is doing well, so why is the stock market always falling?" This question was fired at me, somewhat aggressively, by an ageing relative whom I cannot answer back in the same tone.

When I dug into her reasons for thinking that the stock market was always falling, it turned out that, based on her information inputs, this was the correct conclusion to draw. You see, she has no interest in investments and, indeed, no need for any such interest because others in her family take care of all financial matters. The only financial news she sees are the headlines that Google puts on the news notifications feature of her phone. These headlines always appear only when the markets have fallen sharply, although I'm not sure whether this choice is algorithmic or some editorial selection.

What is undoubtedly true is that outside the financial newspapers and websites, the stock markets make it to the headlines only when there is a sharp one-day drop of the main indexes, generally by at least 2 per cent. There seems to be a sharp bad-news-only filter at work when it comes to stock market news. These headlines then get amplified by whatever logic (or lack of it) dictates what gets thrown on people's phone screens. Those of us who are serious investors hardly ever pay any attention to one-day swings in stock prices and indexes. However, people who are just bystanders and those who are newcomers to the markets do get influenced by this fear-inducing news system.

On social media, too, there seems to be an entire subculture of 'research' analysing one-day returns, in which counting the number of sharply negative days seems to feature prominently. To be fair, since the primary goal of social media is to gain attention, this does seem to work. I guess it's also possible that day traders and short-term punters imagine these vacuous observations to be actually useful, but I would have no idea about that.

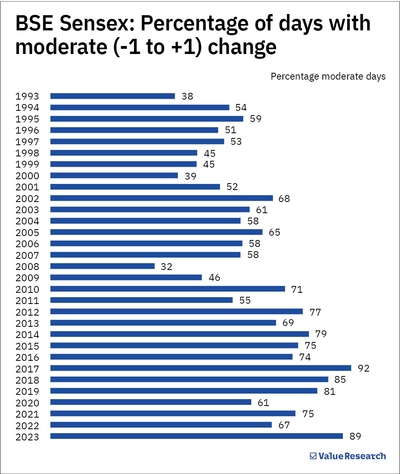

Anyhow, I was sufficiently intrigued by this whole business so I did a small investigative exercise on Value Research's analytical platform on the BSE Sensex. I looked at daily closing values from 1993 to 2023 and obtained a count of the number of trading days under five categories of daily returns: worse than -2 per cent, -1 to -2 per cent, -1 to +1 per cent, +1 to +2 per cent and better than +2 per cent. When I look at this data, it's quite noticeable that the number of days that could make one fearful (a drop worse than 2 per cent) have gone down sharply over the years. Here's that series of the number of sharply negative days, starting with 1993 and ending with 2023: 25, 11, 14, 20, 18, 31, 20, 49, 25, 7, 8, 18, 8, 25, 17, 63, 28, 9, 15, 4, 6, 1, 10, 6, 0, 5, 2, 23, 5, 9, and 0. The effect is most notable when comparing years that are sharply positive. For example, take 1999, when the market was up a huge 75 per cent, the highest in the entire sample. The Sensex started the year at 3060 and ended at 5375. And yet, during this year, there were 20 trading days when it fell by more than 2 per cent, including one day when it fell 6.9 per cent!

Contrast this with the three years of 2021-23 when the Sensex gained a cumulative 50 per cent and yet the total such days were only 14. Or the four years of 2016-2019 when the markets were up a cumulative 57 per cent and yet there were only 13 total days when they fell more than 2 per cent. The standout conclusion of my analysis is that the markets are much calmer now than they used to be. This is best seen in the middle 'moderate' band, the one from -1 to +1 per cent. The average number of days in this range from 1993 to 2009 is 126, while from 2010 to 2023 is 186!

I would say that we have seen a massive moderation of the volatility of the stock markets. However, the general impression is that the markets are more volatile, risky and prone to collapses. What's more, the negative impact of this is not limited to just to people like my aunt. It also lies at the root of, to take just one example, the persistent refusal to increase equity investments in NPS and EPF.

Personally, I lay the blame squarely at the feet of the news media and social media. This fake news about how volatile and risky the equity markets are is doing a lot of serious damage.

Also read: Share price misconceptions