One97 Communications, famously known as Paytm, faced a major blow recently when the Reserve Bank of India (RBI) issued a circular prohibiting it from offering banking services. As a result, its stock plummeted around 36 per cent in just two days!

RBI's directive

The RBI banned Paytm from offering all forms of banking services due to issues of non-compliance and material supervisory concerns.

Effective February 29, Paytm Payments Bank will no longer be able to accept new users, and even the existing users will be unable to utilise Paytm wallets, Fastags, and mobility cards after this date. The ban extends to other banking services, such as the transfer of funds, UPI, and immediate payment services. However, withdrawals will be possible.

Repeated violations

This is not the first time Paytm has flouted regulatory guidelines.

In June 2018, an RBI audit prohibited Paytm Payments Bank to onboard new customers due to KYC process issues.

Further, RBI had also imposed a penalty of Rs 1 crore in October 2021 and Rs 5 crore in October 2023 for misrepresentation and non-compliance with licensing guidelines and cybersecurity measures.

In March 2022, the bank was again directed to cease onboarding immediately due to continued non-compliance issues.

In November 2023, RBI instructed banks and NBFCs to increase the risk weightage on consumer credit by 25 percentage points to 125 per cent. As a result, Paytm had to halt its 'buy now, pay later' services and reduce its loan exposure below Rs 50,000.

Business impact

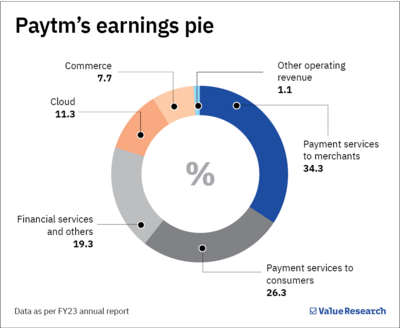

This directive by RBI will significantly impact Paytm's revenue and profitability. It will disrupt its loan disbursal process and significantly affect its operation. Additionally, merchant relations have to be revised, and the integrated services (that were Paytm's key attractions) will have to be suspended as point-of-sale services, wallets, UPI, and other services are linked with Paytm Payments Bank.

In a worst-case scenario, the revenue could drop up to 30 per cent to Rs 7,032 crore since the entire merchant transactions base is treading on thin ice. As per management, the EBITDA (earnings before interest, taxes, depreciation, and amortisation) could fall between Rs 300 - 500 crore. This could increase the company's EBITDA-based losses by 37-62 per cent.

Investors corner

Paytm was already in the bad books of many investors due to its inconsistent cash flow and loss-making nature. The reliance on its payments bank as a growth driver is now in jeopardy.

Investors who bought Paytm shares in the IPO would have faced a 77 per cent loss to date.

Despite the management's intentions to address this issue, it is clear that there will be a substantial impact on the company's operations. With the loss of its primary growth driver, the future of Paytm appears bleak.

Investors may be tempted to buy Paytm now as it appears to be available 'cheap', but they must remember that it is a loss-making, cash-burning, and, now, a growth driver-less company.

Also read: Polycab's high-voltage scandal