If you are reading this article, you must have some interest in finance and you might have come across the business newspaper, Mint. What if we tell you that the company which owns this newspaper is available for free in the market?

Surprised?

Well, the company we are talking about is HT Media, whose market cap is currently less than the value of the cash on its books. The company trades at a market cap of Rs 740 crore (as of February 27, 2024), almost similar to the net cash (including mutual fund investments) of Rs 754 crore (as of December 2023) in its balance sheet.

In layperson's terms, the market is simply not interested in HT Media's business and that all its media assets and real estate properties seem to be available for free.

How is the book valued?

HT Media is not even worth half of its net worth

| Company | Market cap (Rs cr) | P/B ratio |

|---|---|---|

| HT Media | 712 | 0.4 |

| Sandesh | 974 | 0.8 |

| DB Corp | 5137 | 2.4 |

| Jagran Prakashan | 2560 | 1.7 |

| Data as of February 28, 2024 | ||

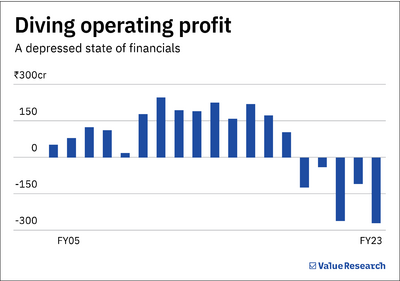

Although market caps exceeding net cash are common sightings in a bear market, even the current bullish market has failed to revive HT Media's fortunes. Let's find out why this rich-in-content business has been reduced to a rag in recent years.

Taking a digi-toll

Digital has hamstrung HT Media to an extent.

Sure, vast swathes of the country still prefer reading physical newspapers, but the company largely caters to an English-speaking audience that is more comfortable with technology. As such, their core readership moved to digital platforms, evidenced by Hindustan Times and Mint's sagging revenues in recent years.

Change in circulation and advertising revenue (FY17-23)

English dailies have been more affected than regional ones

| Company | Change (%) |

|---|---|

| HT Media* | -44.2 |

| Hindustan Media Ventures** | -27.8 |

| Jagran Prakashan | -20.6 |

| Sandesh | -6.7 |

| DB Corp | -0.2 |

|

*HT Media Standalone includes Hindustan Times and Mint **Hindustan Media Ventures include the Hindi newspaper |

|

Rising printing costs and a flop radio venture further knocked the wind out of their sails.

Additionally, their foray into the digital job market through Shine (a job-seeking portal) has yet to work out. It's been over a decade, and they are still nowhere close to the market leader, Naukri. One of the reasons we could find was the very low subscription fees, which made it easy for fraudsters to enter this platform and affect its credibility.

Management flip-flops

The New Delhi-based company was on the front foot in the mid-2000s. It had ventured into India's relatively untapped digital market by launching Shine, Desimartini (a movie review and content platform), and HTCampus (a college application portal) in rather quick succession.

But it started unravelling when it merged all its digital portals under a separate entity called Digicontent. It moved the entire content team (even the Hindustan Times and Mint teams) there to lower its employee costs on its books. But that was a mere window-dressing exercise, as HT Media continues to purchase content from Digicontent on a contractual basis to this day. If you count the content sourcing fees, their employee cost still remains one of the highest in the industry.

Employee costs vs peers (FY23)

HT Media's employee costs are the highest among its peers

| Employee cost (Rs cr) | Employee cost (% of revenue) | |

|---|---|---|

| HT Media* | 543 | 31.7 |

| DB Corp | 387 | 18.2 |

| Jagran Prakashan | 389 | 21 |

| *Including content sourcing fees | ||

To worsen matters, the company has failed to contain its other expenses as well. Legal and Professional Expenses—which form a major part of its expenditures but do not even appear as a line item for its peers—Repair and Maintenance, Travel, and Marketing Costs remain among the highest among its peers.

Poor cost control

Other expenses as a % of revenue in FY23. As you can see, HT Media's costs are higher in all the below metrics.

| Costs | HT Media | DB Corp | Jagran Prakashan |

|---|---|---|---|

| Marketing | 8.5 | 1.8 | 3.4 |

| Repair and manintenance | 3.3 | 1.5 | 2.0 |

| Travel | 2.8 | 1.0 | 0.9 |

| Communication | 0.7 | 0.3 | 0.3 |

| Insurance | 0.4 | 0.1 | 0.2 |

At one point, the management did try to Control+Z their merger move by offering its investors four HT Media shares for every 13 Digicontent shares at a time when their share prices were almost at similar levels. Needless to say, the company's proposal was booted out by their shareholders.

Our take

Not everything available at a discount carries value. If problems mentioned above persist, the share price may continue to nosedive. HT Media has been trading at less than its book value since June 2018 and seen its share price tumble 65 per cent.

While investors can hope for a one-time dividend or a buyback to profit from their investment, it remains a pipedream. Instead of spreading the love among its shareholders, the management has preferred investing its surplus cash in startups such as Oyo and Mobikwik.

Is it any wonder that the company has failed to create wealth for shareholders?

Also read: This dividend stock recently became a wealth creator